- 262 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

The Low Cost Carrier Worldwide

About this book

Low Cost Carriers (LCCs) have become an integral part of today's air transport and tourism industries. Originating in the United States, the low-cost concept has subsequently been adopted by airlines on all continents. LCCs in Europe and North America, and to some extent in Asia, have already been well covered by academic literature. However, scientific publications on the topic of LCCs in Africa, Latin America, the Middle East, Australia and New Zealand are scarce. This volume provides the first comprehensive overview of developments, the legal framework and the current situation of the low-cost carrier phenomenon across the globe. It contains a dozen chapters, each dedicated to a region, all written by highly experienced and renowned experts from around the world. The Low Cost Carrier Worldwide is written primarily for upper-level undergraduate and postgraduate students, as well as researchers and practitioners within the fields of aviation, transport and tourism.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

PART I

Introduction

Chapter 1

The Low Cost Carrier – A Worldwide Phenomenon?!

Introduction

An overview of the low cost carriers (LCCs) operating within the worldwide air traffic market becomes outdated (almost) as quickly as editions of a daily newspaper over the course of the day of publication. Nonetheless, from both an academic and a practitioner’s perspective it is not only interesting but also important to gain an insight into LCC developmental trends, possible continental differences and the identification of typical elements of the low cost business model.

The following analysis is based on a comprehensive review of publicly available information regarding the worldwide operation of LCCs and information gathered from industry publications.1 Furthermore, individual LCCs were contacted via telephone and/or email for clarification purposes or to gain additional information.

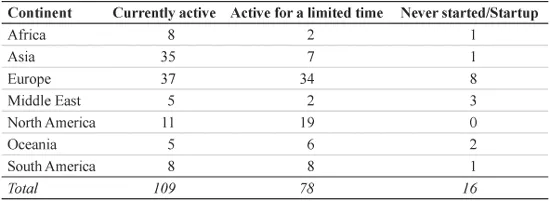

Classification of airlines according to the low cost model was also based on industry publications (see Note 1). It was determined whether the airlines were currently operating and whether they applied typical characteristics of low cost business models. Typical regional airlines acting as feeder airlines within local markets (such as Egypt Air Express and American Eagle) and charter airlines (such as Air Holland, Condor and TUIfly) were not included in the analysis. However, some airlines have developed into a hybrid model, for example Air Berlin serves typical low cost routes, yet also offers long haul flights as well as typical tourist routes, usually served by charter airlines. Furthermore, while Aer Lingus operates as a LCC within the European market, it more closely resembles a full service carrier (FSC) on long haul flights; such hybrid carriers were included for the purpose of this analysis. Subsequently, 109 LCCs2 currently active in the worldwide market were identified.

Table 1.1 Numbers of low cost carriers per continent (2011)

Additionally, 94 LCCs were identified which were either active for a limited time (78), or announced their intentions but never actually carried out flight operations (16). Table 1.1 illustrates the LCCs included in the current analysis grouped according to continents. The majority of currently active LCCs are operating in Europe and Asia.

Development of the Low Cost Carrier

As is the case with many developments within air transportation, the LCC concept originated in the USA. Until the mid-1970s, the regulatory provisions of the aviation market were based on the Civil Aviation Act of 1938, which codified strict regulations regarding market access and price controls. The strict regulations resulted in exorbitant prices, distorted pricing structures to the detriment of long haul flights, and brought about an intensive and costly competition over quality (Aberle 2003). In the early 1960s the former US Civil Aeronautics Board (CAB) first approved the variation of promotional fares based on time of day, length of stay, or type of travel. However, the market remained rather rigid and it was not until the early 1970s that greater flexibility was achieved. This was due mainly to the introduction of new types of aircraft (such as the Boeing B747, which doubled the available seating capacity in comparison to the previously used aircraft); and the increasing activity of charter airlines, which entered the market with extremely low fares. In the 1970s the CAB deregulated the American aviation market. Due in particular to pressure exerted by charter airlines wishing to sell their fares without the requirement to sell packages including additional travel services, the American aviation market was deregulated by the CAB in the 1970s.

While in 1975 the CAB eased regulations regarding market access, in 1978 an important milestone was achieved with the ratification of the Airline Deregulation Act (Pompl 2007). Important transportation policy objectives were to increase competitiveness through liberalization of market access; to achieve greater flexibility of pricing structures by eliminating requirements; and to bring about greater adaptability of the airlines to current market conditions (Aberle 2003).

Based on the economic developments, the resulting increase in demand for air travel, and the deregulation of the market, there was an increase in competitiveness within the aviation market. Former charter airlines and new start-ups entered the market as LCCs, often offering dumping prices, and engaged in direct competition with the traditional (FSCs).

It is rather difficult to pinpoint the origins of LCCs since opinions in the literature differ (see also Figure 2.1 in Chapter 2 of this volume). For example, Pacific Southwest Airlines (PSA) founded in 1949 as a Californian intrastate carrier, was transformed into an LCC in the early 1960s; unfortunately, due to poor strategic decision making and investments PSA was bankrupt by the mid-1970s (Bailey, Graham and Kaplan 1985).

Southwest Airlines, founded in 1967 and since developed into one of the largest airlines in the world, is also regarded as one of the pioneers in the low cost sector. Southwest started operations on 18 June 1971 and decided against the conventional network and hub system, instead opting for easily implementable point-to-point services (Bjelicic 2004, Knorr 2007).

Following Southwest Airlines, further LCCs were founded in the USA such as American TransAir (1972) and Midwest Express (1984), while already established companies entered the low cost market with subsidiary enterprises.3 In 1972, the British Laker Airways intended to enter the low cost segment with a ‘Skytrain’ operating between London and New York, but operations did not begin until 1977 when Laker received traffic rights for the United States. Thereafter further LCCs such as Braniff (1979), Virgin Atlantic (1984) and People Express (1983), began operations in the low priced air traffic segment between the two continents. Although the concept was not economically successful – with the exception of Virgin Atlantic all other airlines exited the market – it significantly changed the market (Pompl 2007).

Growth vs Decline

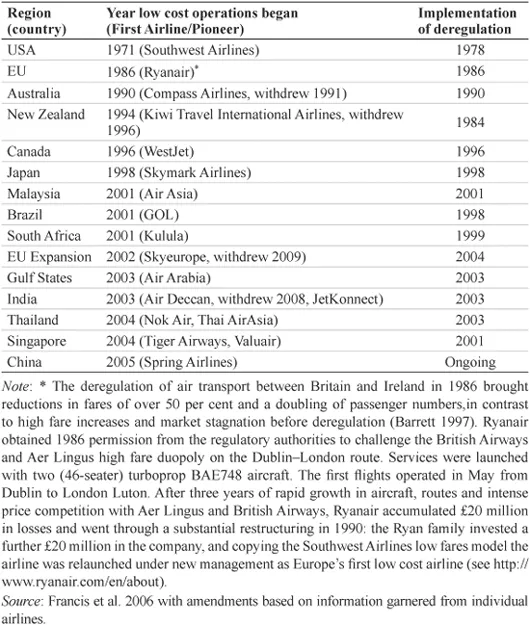

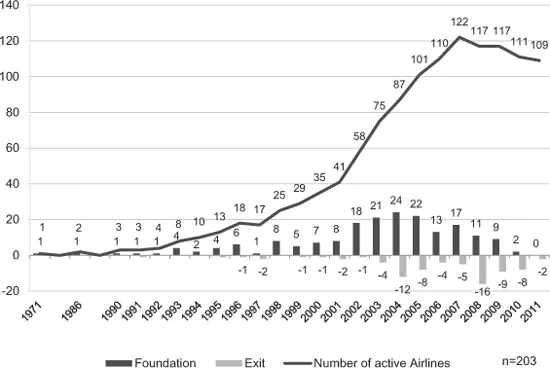

The respective deregulation processes had an accelerating effect, so that during the 1990s and 2000s LCCs gradually established themselves on all continents. As shown in Table 1.2, there were two decisive time periods for the development of LCCs: the early to mid-1990s in Canada, Europe and Oceania; and the 2000s in Asia, Eastern Europe and the Middle East. Thus, it is of no great surprise that most LCC start-ups were launched within these time periods (see Figure 1.1). As has previously been mentioned, 94 LCCs are no longer active or were founded but never fully began operations.4 From Figure 1.1 it is clear that most of the companies exited the market within the period 2004–2005 and during the global economic crisis (2008–2009). The most LCCs were recorded before the global economic crisis. Interestingly, there were also many new start-ups during the middle of the decade, which can be attributed to the worldwide expansion of the low cost business model previously described.

Table 1.2 The beginning of deregulation and low cost developments by regions

Figure 1.1 Number of market entries and exits of low cost carriers

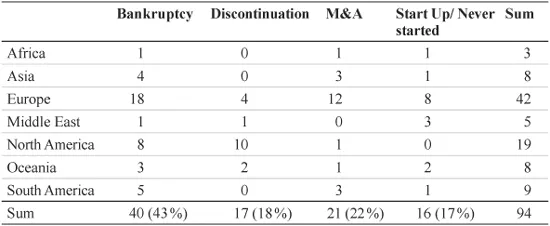

Within this context the reasons cited for exiting the market are also of interest. As can be expected, financial problems are of the utmost importance: 43 per cent of the companies which exited the market did so due to bankruptcy. The suspension of operations among LCCs due to economic deficits/red figures/high losses takes second place (18 per cent). This measure was often taken in connection with the establishment of a low cost subsidiary by a FSC (often referred to as carrier within carrier), as well as a restructuring of the airline, i.e. a modification of the business model to charter or to a FSC. Other reasons are mergers and acquisitions (M&A) through another airline (22 per cent).

Table 1.3 Number of market exits and their reasons by continent (1991–2011)

Additionally, 16 airlines were identified which never started flight operations and have since disappeared from the market (never started) or are listed as startups (mid-2011) and are preparing flight operations (see Table 1.3 on the previous page).

A detailed examination of the companies exiting the aviation market reveals that the greatest fluctuation took place within the European market; almost half of the companies exiting the LCC market can be found in this region. Furthermore, approximately two-thirds of the airlines that never commenced operations can be found in the combined markets of the Europe and the Middle East.

Analysis of Corporate Organization: Newcomer Versus Subsidiary Airlines

Some LCCs founded further airlines as subsidiary companies and have been fairly successful. For example, the Virgin Group operates as an FSC (Virgin Atlantic) and low cost subsidiaries in Oceania (Virgin Australia) and America (Virgin America).

Over the last few years some FSCs have also founded their own subsidiaries or had holdings/shares in LCCs (see Table 1.4). This measure was tak...

Table of contents

- Cover Page

- Half Title page

- Title Page

- Copyright Page

- Contents

- Figures

- Tables

- List of Contributors

- Preface

- List of Abbreviations

- Introduction

- Europe

- The Americas

- Asia and Oceania

- Africa and the Middle East

- Conclusion

- Appendix 1.1 List of Currently Operating Low Cost Airlines (109)

- Appendix 1.2 List of Former Low Cost Airlines

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Low Cost Carrier Worldwide by Sven Gross,Michael Lück in PDF and/or ePUB format, as well as other popular books in Technology & Engineering & Business General. We have over 1.5 million books available in our catalogue for you to explore.