Nearly every day brings news of another merger or acquisition involving the companies that control our food supply. Just how concentrated has this system become? At almost every key stage of the food system, four firms alone control 40% or more of the market, a level above which these companies have the power to drive up prices for consumers and reduce their rate of innovation. Researchers have identified additional problems resulting from these trends, including negative impacts on the environment, human health, and communities.

This book reveals the dominant corporations, from the supermarket to the seed industry, and the extent of their control over markets. It also analyzes the strategies these firms are using to reshape society in order to further increase their power, particularly in terms of their bearing upon the more vulnerable sections of society, such as recent immigrants, ethnic minorities and those of lower socioeconomic status. Yet this study also shows that these trends are not inevitable. Opposed by numerous efforts, from microbreweries to seed saving networks, it explores how such opposition has encouraged the most powerful firms to make small but positive changes.

- 216 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Chapter 1

Food system concentration: a political economy perspective

Power is not a means, it’s an end.

—O’Brien (Nineteen Eighty-Four)

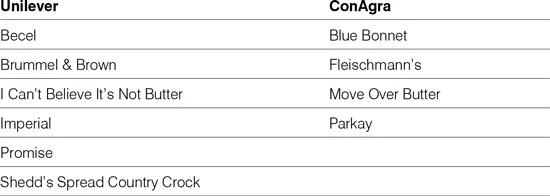

If you go into a typical grocery store in the United States and make your way back to the margarine case, you will probably see approximately a dozen different brands. If you look very closely at the packaging, however, you may find a small seal, which signifies the majority of these are owned by either Unilever or ConAgra (Table 1.1). Although these two firms dominate the margarine market—Unilever accounts for 51.2 percent of sales in the US market and ConAgra for 16.9 percent (Grocery Headquarters 2013)—their power is hidden from us through an illusion of numerous competing brands. Margarine is not a unique case, and while the number of options offered may differ, similar patterns can be found in almost every food or beverage category. The bread shelves, for example, may provide slightly more choices, but this conceals the fact that Grupo Bimbo and Flowers Foods each own more than a dozen leading brands and together control approximately half of the US market (Thomas and Cavale 2013). The wine aisle may contain literally hundreds of brands, but it is very difficult to discern that scores of these, as well as more than half of US sales, are controlled by only three companies: Gallo, The Wine Group, and Constellation (Howard et al. 2012). In nearly every other stage of the food system, including retailing, distribution, farming and farm inputs (e.g., seeds, fertilizers, pesticides), a limited number of firms or operations tend to make up the vast majority of sales.

Table 1.1 Ownership of margarine brands

Is this a problem? An increasing number of people argue that indeed it is: the firms that dominate these industries are criticized for a long list of purported negative impacts on society and the environment. Just a few examples include:

• Walmart, which controls 33 percent of US grocery retailing, is challenged for exploiting its suppliers, taking advantage of taxpayer subsidies, and paying extremely low worker wages.

• McDonald’s, which controls more than 18 percent of US fast food sales, is also critiqued for extremely low wages, as well as the negative health consequences and environmental impacts of its products.

• Tyson, which controls more than 17 percent of US chicken, pork, and beef processing is reproached for its pollution, poor treatment of farmers, and contributions to the decline of rural communities.

• Monsanto, which controls 26 percent of the global commercial seed market, is denounced for its influence on government policies, spying on farmers it suspects of saving and replanting seeds, and the environmental impacts of herbicides tied to these seeds.

These impacts tend to disproportionately affect the disadvantaged—such as women, young children, recent immigrants, members of minority ethnic groups, and those of lower socioeconomic status—and as a result, reinforce existing inequalities (Allen and Wilson 2008). Like ownership relations, the full extent of these consequences may be hidden from public view.

This book seeks to illuminate which firms have become the most dominant, and more importantly, how they shape and reshape society in their efforts to increase their control. These dynamics have received insufficient attention from academics and even critics of the current food system. The power of dominant firms extends far beyond narrow economic boundaries, for example, providing them with the ability to damage numerous communities and ecosystems in their pursuit of higher than average profits. The social resistance provoked by these negative consequences is another area that is less visible to the majority of the population. When such resistance is evident at all, it frequently appears insignificant, failing to challenge the direction of current trends. Even very small movements, however, may influence which firms end up winners or losers or close off particular avenues for growth. These accomplishments also suggest potential limits and therefore the possibility that dominant firms may experience much greater threats to their power in the future.

Increasing concentration

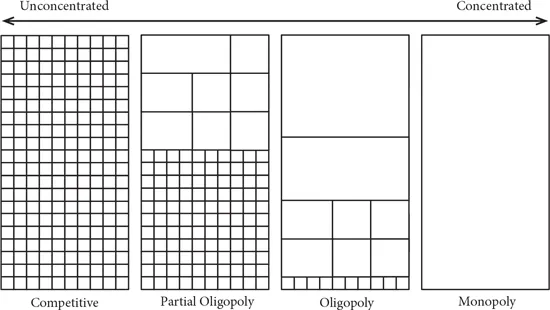

Concentration is a term used to describe the composition of a given market, and especially its potential impacts on competition. At one end of the spectrum are markets that are described as unconcentrated or fragmented, which economists consider to be freely competitive (Figure 1.1). In this type of market, sellers are “price takers” and lack the ability to raise prices. At the other end of the spectrum are concentrated markets, which in their most extreme form are monopolies controlled by just one firm. In these situations there are no alternatives, and the monopolists have substantial power to raise prices without losing customers. Also at this end of the spectrum are oligopolies, in which markets are dominated by several large firms but are characterized by very limited forms of competition; these are sometimes described by critics as “shared monopolies” (Bowles, Edwards, and Roosevelt 2005, 265). In the middle are partial oligopolies, in which large firms may have some control over their prices but lack the power to significantly reduce competition, as is the case with oligopolies. The word monopoly is derived from the Greek words for single (mono) and seller (polein), but concentrated markets may also occur among buyers, as found in a monopsony or oligopsony (derived from the Greek word for buy, opsōnía).

Figure 1.1 Levels of market concentration.

Each rectangle represents a single, hypothetical firm, with size proportional to market share.

There has been a strong tendency in more industrialized countries, including the United States, to move away from competitive markets and toward higher levels of concentration (Heffernan, Hendrickson, and Gronski 1999; Du Boff and Herman 2001). As markets go through this process of consolidation, the average firm size increases, barriers to entry for other firms rise, and the remaining firms have more influence over prices, as well as a greater potential for higher profits. These are some of the widely recognized reasons why markets tend to become less competitive—firms understand the benefits to be gained by expanding their market share, reducing the number of competing firms, and increasing their leverage over the terms of exchange (Foster and McChesney 2012). These trends are most evident in industries such as airlines and telecommunications, in which the US government intervened to encourage greater competition, only for them to eventually return to more oligopolistic structures (Brock 2011).

Potential negative impacts

Governments sometimes intervene when industries reach a high level of concentration because such limited competition may lead to numerous negative outcomes. Market consequences could include consumers paying higher prices, suppliers receiving lower prices, or reduced innovation. Oligopolistic firms have disincentives to reduce profits by investing in research and development, particularly when doing so could lead to lower barriers to entry and increasing competition. In addition, large organizational size can discourage innovation indirectly, via complex bureaucracies that are reluctant to approve new ideas (Brock 2011). Increasing size can be an advantage for reducing prices paid for inputs, however, as smaller suppliers may have fewer alternative buyers for their products and less organizational capacity to negotiate the best possible terms (Calvin et al. 2001).

In order to raise consumer prices, it is not necessary for executives to gather in one room and conspire to achieve these markups. When just a few firms control a large share of the market, they can simply indicate their intention to raise prices, and the others will benefit by following suit, a strategy that is called price signaling (Baran and Sweezy 1966). Oligopolistic firms can more easily pressure each other to avoid price wars that would lower their profits. The result is an unwritten rule that rivalries based on advertising, product differentiation, and reducing labor costs are expected, but competing on price is unacceptable. John Bell, a former CEO of a coffee company that was eventually acquired by Kraft, explained that he was constantly reinforcing this message to rivals through his speeches and media interviews in order to prevent “the natural competitive reaction.” Lowering prices was given the code word “non-strategic” in public communications, and emphasizing his opposition to it was “an indirect means of telling competition to ‘play ball’ (Bell 2012).”

Nevertheless, executives in industries controlled by a small number of firms may go beyond signaling and are occasionally even caught conspiring to fix prices. A few examples include:

• The US Federal Trade Commission (FTC) discovered in the mid-1960s that leading bakeries and retailers in Washington State had met frequently and agreed to increase the price of bread by 15–20 percent (Parker 1976).

• In 2013, Hershey pleaded guilty to working with other large chocolate manufacturers (Mars, Nestlé, and Cadbury) to raise prices in Canada. While the other firms denied the charges, together they paid more than $22 million to settle a resulting class-action lawsuit (Culliney 2013).

• Western European governments have reported numerous schemes to raise food prices in recent years (e.g., beer, flour, bananas, chocolate and dairy products), which have resulted in fines totaling hundreds of millions of dollars.

As mentioned above, additional problems may result from increasing concentration in the food industry, including negative impacts on communities, labor, human health, animal welfare and the environment (economists define many of these impacts as “externalities”).

Regardless of the consequences, as industries consolidate, fewer and fewer people have the power to make important decisions, such as what is produced, how it is produced, and who has access to these products (Heffernan, Hendrickson, and Gronski 1999). Dominant firms are typically controlled by a small board of directors (eleven people on average), with decision-making power concentrated in the hands of the chief executive officer (CEO). The individuals who serve on these boards typically do not reflect the composition of society and in the United States are most often men, of European ethnicity, with an average age of 60 and educated at elite institutions like Ivy League schools (Lyson and Raymer 2000). They also tend to share very similar conservative worldviews through frequent socializing with other members of the upper class in exclusive clubs, summer resorts, philanthropic organizations, etc. (Domhoff 2014).

Unanswered questions

Despite its adverse impacts on society at large, increasing market concentration is frequently portrayed as unstoppable. Business historian Louis Galambos, for example, claims that, “Global oligopolies are as inevitable as the sunrise” (Zachary 1999). Scientists who study social networks, including business networks, have pointed to a tendency for the “rich to get richer” as their initial advantages are magnified and eventually snowball, leading to even greater success (Barabási and Bonabeau 2003; Easley and Kleinberg 2010). Yet these trends have been highly uneven temporally, geographically, and by position within the food system (Friedland 2004). The farming of commodity crops in the Midwestern United States or the regional distribution of many specialized foods, for example, can still be characterized as competitive markets, suggesting that establishing and maintaining an oligopoly is not always as easy as claimed (Lewontin and Berlan 1986; Lewontin 2000).

The interesting question, then, is why have some segments of the food system already become oligopolies and not others? Why don’t they all resemble the global soft drink industry, which has been dominated by just two firms, Coca-Cola and Pepsi, for decades? This suggests additional questions, such as what specific factors currently constrain other food and agriculture industries from approaching this organizational model? What factors might enable them? The answers are important because they might help slow, or even reverse, current trends toward concentration. Even if they don’t take us quite that far, a better understanding of how concentration occurs could help us to shape its direction and ameliorate some of its negative impacts.

Before answering these questions, however, a critical first step is simply to characterize the changes that have taken place, which can be more difficult than it sounds. Determining the level of concentration in different food industries is complicated by the inaccessibility of accurate sales data (Heffernan, Hendrickson, and Gronski 1999; Fernandez-Cornejo and Just 2007), even for “publicly” held firms. Uncovering just who owns what is also challenged by the opaque and constantly shifting corporate parentage of many brands and subsidiaries. Due to increasing public concern about food issues—evidenced by bestselling books by Eric Schlosser, Michael Pollan, and Barbara Kingsolver, and numerous documentary films that critique the current food system—some firms are taking increasing measures to hide their dominance. Trade journals are less likely to report market shares for leading food and agricultural firms, for example, and the types of acquisitions that typically generated press releases in the late 1990s may now go unannounced.

Differing perspectives

Economics

Industry concentration is studied primarily by economists. One simple indicator that they developed to characterize the competitiveness of markets is a concentration ratio or the sum of the market shares of the top firms. A frequently used number is the top four, sometimes abbreviated as a CR4. Thresholds vary depending on the analyst, but most institutional economists suggest that when four firms control more than 40 percent or 50 percent of a market, it is no longer competitive (Scherer and Ross 1990; Shepherd and Shepherd 2004). A more recent measure, used by regulators such as the US Department of Justice (DOJ) to evaluate mergers and acquisitions, is the Herfindahl-Hirschman Index (HHI). The index is the sum of squares of market share for all the firms in a given market. If one firm, for example, controlled 100 percent of a market, the HHI would be 100 squared, or 10,000. If two firms divided the market, the HHI would be 5,000 (50 squared + 50 squared). The US government once considered markets with an HHI above 1,800 to be highly concentrated (Gould 2010). Notably, this level would not be exceeded if four equally sized firms controlled 80 percent of the market, despite the highly conducive environment for price signaling that would result. In 2010, the DOJ and the FTC raised the threshold even higher, to 2,500—the equivalent of four firms evenly dividing 100 percent of the market. Although the HHI is designed to be more sensitive to changes in market share among the top firms, it is less intuitive than concentration ratios.

A weakness of both measures is that they are designed to characterize horizontal integration within a national (or smaller than national) market. Concentration is increasingly occurring through vertical integration, however, as firms buy upstream suppliers or downstream retailers, both in national markets and at the global level. In addition to direct ownership, less formal but still effective means of control are becoming more common, such as strategic alliances or contracting arrangements (Heffernan 2000). As a result, the full extent of market power has become much more difficult to establish accurately, and concentration measures may underestimate the ability of firms to enhance their own interests at the expense of others.

Mainstream economists tend to view concentration as unproblematic, due to a strong abstract belief in economies of scale, despite insufficient empirical evidence to support these supposed efficiencies (Johnson and Ruttan 1994; DiLorenzo 1996). Consumers are often claimed to benefit from synergies and lower transaction costs that are expected to result from mergers and acquisitions (Farrell and Shapiro 2001). Because of their organizational c...

Table of contents

- Cover

- Halftitle Page

- Title Page

- Contents

- List of Figures

- Acknowledgements

- 1. Food system concentration: a political economy perspective

- 2. Reinterpreting antitrust: retailing

- 3. Structuring dependency: distribution

- 4. Engineering consumption: packaged foods and beverages

- 5. Manipulating prices: commodity processing

- 6. Subsidizing the treadmill: farming and ranching

- 7. Enforcing the new enclosures: agricultural inputs

- 8. Standardizing resistance: the organic food chain

- 9. Endgame?

- Bibliography

- Index

- Imprint

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Concentration and Power in the Food System by Philip H. Howard in PDF and/or ePUB format, as well as other popular books in Politics & International Relations & Agricultural Public Policy. We have over 1.5 million books available in our catalogue for you to explore.