Delve into the mind of a fraudster to beat them at their own game

Corporate Fraud Handbook details the many forms of fraud to help you identify red flags and prevent fraud before it occurs. Written by the founder and chairman of the Association of Certified Fraud Examiners (ACFE), this book provides indispensable guidance for auditors, examiners, managers, and criminal investigators: from asset misappropriation, to corruption, to financial statement fraud, the most common schemes are dissected to show you where to look and what to look for. This new fifth edition includes the all-new statistics from the ACFE 2016 Report to the Nations on Occupational Fraud and Abuse, providing a current look at the impact of and trends in fraud. Real-world case studies submitted to the ACFE by actual fraud examiners show how different scenarios play out in practice, to help you build an effective anti-fraud program within your own organization. This systematic examination into the mind of a fraudster is backed by practical guidance for before, during, and after fraud has been committed; you'll learn how to stop various schemes in their tracks, where to find evidence, and how to quantify financial losses after the fact.

Fraud continues to be a serious problem for businesses and government agencies, and can manifest in myriad ways. This book walks you through detection, prevention, and aftermath to help you shore up your defenses and effectively manage fraud risk.

Understand the most common fraud schemes and identify red flags

Learn from illustrative case studies submitted by anti-fraud professionals

Ensure compliance with Sarbanes-Oxley and other regulations

Develop and implement effective anti-fraud measures at multiple levels

Fraud can be committed by anyone at any level—employees, managers, owners, and executives—and no organization is immune. Anti-fraud regulations are continually evolving, but the magnitude of fraud's impact has yet to be fully realized. Corporate Fraud Handbook provides exceptional coverage of schemes and effective defense to help you keep your organization secure.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

In the world of commerce, organizations incur costs to produce and sell their products or services. These costs run the gamut: labor, taxes, advertising, occupancy, raw materials, research and development, and, yes—fraud and abuse. The latter cost, however, is fundamentally different from the former: The true expense of fraud and abuse is hidden, even if it is reflected in the profit‐and‐loss figures.

For example, suppose the advertising expense of a company is $1.2 million. But unknown to the company, its marketing manager is in collusion with an outside ad agency and has accepted $300,000 in kickbacks to steer business to that firm. That means the true advertising expense is overstated by at least the amount of the kickback—if not more. The result, of course, is that $300,000 comes directly off the bottom line, out of the pockets of the investors and the workforce.

DEFINING OCCUPATIONAL FRAUD AND ABUSE

The example just given is clear‐cut, but much about occupational fraud and abuse is not so well defined, as we will see. Indeed, there is widespread disagreement on what exactly constitutes these offenses.

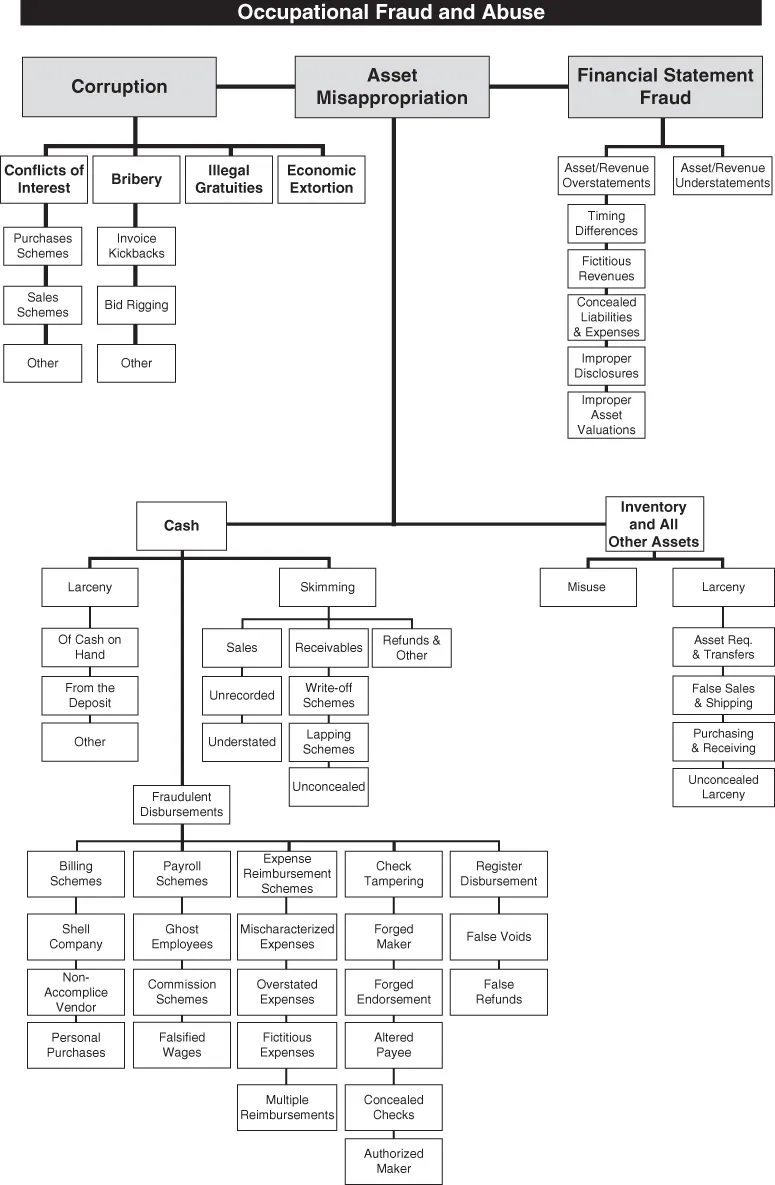

For purposes of this book, occupational fraud and abuse is defined as “the use of one's occupation for personal enrichment through the deliberate misuse or misapplication of the employing organization's resources or assets.”1

This definition's breadth means that it involves a wide variety of conduct by executives, employees, managers, and principals of organizations, ranging from sophisticated investment swindles to petty theft. Common violations include asset misappropriation, financial statement fraud, corruption, pilferage and petty theft, false overtime, use of company property for personal benefit, and payroll and sick time abuses. Four elements common to these schemes were reported by the Association of Certified Fraud Examiners (ACFE) in its first Report to the Nation on Occupational Fraud and Abuse, released in 1996: “The key is that the activity (1) is clandestine, (2) violates the employee's fiduciary duties to the organization, (3) is committed for the purpose of direct or indirect financial benefit to the employee, and (4) costs the employing organization assets, revenues, or reserves.”2

An employee, in the context of this definition, is any person who receives regular and periodic compensation from an organization for his or her labor. The term is not restricted to the rank‐and‐file staff members; it also includes corporate executives, company presidents, top and middle managers, contract employees, and other workers.

Defining Fraud

In the broadest sense, fraud can encompass any crime for gain that uses deception as its principal modus operandi. Of the three ways to illegally relieve a victim of money—force, trickery, or larceny—all offenses that employ trickery are frauds. Thus, deception is the linchpin of fraud.

However, while all frauds involve some form of deception, not all deceptions are necessarily frauds. Under common law, four general elements must be present for a fraud to exist:

A material false statement

Knowledge that the statement was false when it was uttered

Reliance of the victim on the false statement

Damages resulting from the victim's reliance on the false statement

The legal definition is the same whether the offense is criminal or civil; the difference is that criminal cases must meet a higher burden of proof.

Let's assume an employee who worked in the warehouse of a computer manufacturer stole valuable computer chips when no one was looking and resold them to a competitor. This conduct is certainly illegal, but what law has the employee broken? Has he committed fraud? Has he committed theft? The answer, of course, is that it depends. Employees have a recognized fiduciary relationship with their employers under the law. Let's briefly review the legal ramifications of the theft.

The term fiduciary, according to Black's Law Dictionary, is of Roman origin and refers to

One who owes to another the duties of good faith, trust, confidence, and candor.

The term fiduciary relationship is further defined as

A relationship in which one person is under a duty to act for the benefit of the other on matters within the scope of the relationship. Fiduciary relationships—such as trustee‐beneficiary, guardian‐ward, agent‐principal, and attorney‐client—require the highest duty of care.3

So, in our example, the employee has not only stolen the chips; in so doing, he has violated his fiduciary duty. That makes him an embezzler. Embezzlement is defin...

Table of contents

Cover

Title Page

Copyright

Dedication

Table of Contents

Preface

About the ACFE

Chapter 1: Introduction

Part I: Asset Misappropriations

Part II: Corruption

Part III: Financial Statement Fraud

Appendix: Sample Code of Business Ethics and Conduct

Bibliography

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Corporate Fraud Handbook by Joseph T. Wells in PDF and/or ePUB format, as well as other popular books in Business & Managerial Accounting. We have over 1.5 million books available in our catalogue for you to explore.