Navigate equity investments and asset valuation with confidence Equity Asset Valuation, Fourth Edition blends theory and practice to paint an accurate, informative picture of the equity asset world. The most comprehensive resource on the market, this text supplements your studies for the third step in the three-level CFA certification program by integrating both accounting and finance concepts to explore a collection of valuation models and challenge you to determine which models are most appropriate for certain companies and circumstances. Detailed learning outcome statements help you navigate your way through the content, which covers a wide range of topics, including how an analyst approaches the equity valuation process, the basic DDM, the derivation of the required rate of return within the context of Markowitz and Sharpe's modern portfolio theory, and more.

Foire aux questions

Comment puis-je résilier mon abonnement ?

Il vous suffit de vous rendre dans la section compte dans paramètres et de cliquer sur « Résilier l’abonnement ». C’est aussi simple que cela ! Une fois que vous aurez résilié votre abonnement, il restera actif pour le reste de la période pour laquelle vous avez payé. Découvrez-en plus ici.

Puis-je / comment puis-je télécharger des livres ?

Pour le moment, tous nos livres en format ePub adaptés aux mobiles peuvent être téléchargés via l’application. La plupart de nos PDF sont également disponibles en téléchargement et les autres seront téléchargeables très prochainement. Découvrez-en plus ici.

Quelle est la différence entre les formules tarifaires ?

Les deux abonnements vous donnent un accès complet à la bibliothèque et à toutes les fonctionnalités de Perlego. Les seules différences sont les tarifs ainsi que la période d’abonnement : avec l’abonnement annuel, vous économiserez environ 30 % par rapport à 12 mois d’abonnement mensuel.

Qu’est-ce que Perlego ?

Nous sommes un service d’abonnement à des ouvrages universitaires en ligne, où vous pouvez accéder à toute une bibliothèque pour un prix inférieur à celui d’un seul livre par mois. Avec plus d’un million de livres sur plus de 1 000 sujets, nous avons ce qu’il vous faut ! Découvrez-en plus ici.

Prenez-vous en charge la synthèse vocale ?

Recherchez le symbole Écouter sur votre prochain livre pour voir si vous pouvez l’écouter. L’outil Écouter lit le texte à haute voix pour vous, en surlignant le passage qui est en cours de lecture. Vous pouvez le mettre sur pause, l’accélérer ou le ralentir. Découvrez-en plus ici.

Est-ce que Equity Asset Valuation est un PDF/ePUB en ligne ?

Oui, vous pouvez accéder à Equity Asset Valuation par Jerald E. Pinto en format PDF et/ou ePUB ainsi qu’à d’autres livres populaires dans Negocios y empresa et Inversiones y valores. Nous disposons de plus d’un million d’ouvrages à découvrir dans notre catalogue.

After completing this chapter, you will be able to do the following:

describe characteristics of types of equity securities;

describe differences in voting rights and other ownership characteristics among different equity classes;

distinguish between public and private equity securities;

describe methods for investing in non-domestic equity securities;

compare the risk and return characteristics of different types of equity securities;

explain the role of equity securities in the financing of a company’s assets;

distinguish between the market value and book value of equity securities;

compare a company’s cost of equity, its (accounting) return on equity, and investors’ required rates of return.

1. Introduction

Equity securities represent ownership claims on a company’s net assets. As an asset class, equity plays a fundamental role in investment analysis and portfolio management because it represents a significant portion of many individual and institutional investment portfolios.

The study of equity securities is important for many reasons. First, the decision on how much of a client’s portfolio to allocate to equities affects the risk and return characteristics of the entire portfolio. Second, different types of equity securities have different ownership claims on a company’s net assets, which affect their risk and return characteristics in different ways. Finally, variations in the features of equity securities are reflected in their market prices, so it is important to understand the valuation implications of these features.

This chapter provides an overview of equity securities and their different features and establishes the background required to analyze and value equity securities in a global context. It addresses the following questions:

What distinguishes common shares from preference shares, and what purposes do these securities serve in financing a company’s operations?

What are convertible preference shares, and why are they often used to raise equity for unseasoned or highly risky companies?

What are private equity securities, and how do they differ from public equity securities?

What are depository receipts and their various types, and what is the rationale for investing in them?

What are the risk factors involved in investing in equity securities?

How do equity securities create company value?

What is the relationship between a company’s cost of equity, its return on equity, and investors’ required rate of return?

The remainder of this chapter is organized as follows. Section 2 provides an overview of global equity markets and their historical performance. Section 3 examines the different types and characteristics of equity securities, and Section 4 outlines the differences between public and private equity securities. Section 5 provides an overview of the various types of equity securities listed and traded in global markets. Section 6 discusses the risk and return characteristics of equity securities. Section 7 examines the role of equity securities in creating company value and the relationship between a company’s cost of equity, its return on equity, and investors’ required rate of return. The final section summarizes the chapter.

2. Equity Securities in Global Financial Markets

This section highlights the relative importance and performance of equity securities as an asset class. We examine the total market capitalization and trading volume of global equity markets and the prevalence of equity ownership across various geographic regions. We also examine historical returns on equities and compare them to the returns on government bonds and bills.

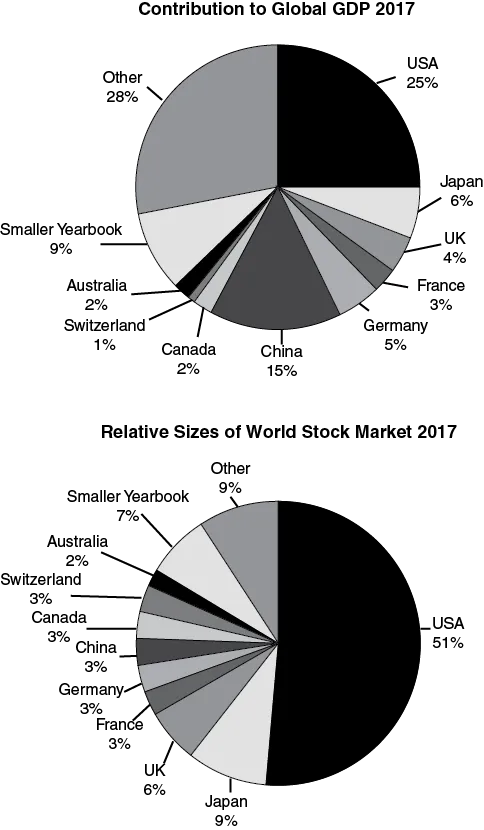

Exhibit 1 summarizes the contributions of selected countries and geographic regions to global gross domestic product (GDP) and global equity market capitalization. Analysts may examine the relationship between equity market capitalization and GDP as a rough indicator of whether the global equity market (or a specific country’s or region’s equity market) is under-, over-, or fairly valued, particularly compared to its long-run average.

Exhibit 1 illustrates the significant value that investors attach to publicly traded equities relative to the sum of goods and services produced globally every year. It shows the continued significance, and the potential overrepresentation, of US equity markets relative to their contribution to global GDP. That is, while US equity markets contribute around 51 percent to the total capitalization of global equity markets, their contribution to the global GDP is only around 25 percent. Following the stock market turmoil in 2008, however, the market capitalization to GDP ratio of the United States fell to 59 percent, which is significantly lower than its long-run average of 79 percent.

As equity markets outside the United States develop and become increasingly global, their total capitalization levels are expected to grow closer to their respective world GDP contributions. Therefore, it is important to understand and analyze equity securities from a global perspective.

Exhibit 1 Country and Regional Contributions to Global GDP and Equity Market Capitalization (2017)

Source: The World Bank Databank 2017, and Dimson, Marsh, and Staunton (2018).

Exhibit 2 lists the top 10 equity markets at the end of 2017 based on total market capitalization (in billions of US dollars), trading volume, and the number of listed companies.1

Note that the rankings differ based on the criteria used. For example, the top three markets based on total market capitalization are the NYSE Euronext (US), NASDAQ OMX, and the J...