Unexpected Discoveries in Issuance, Investment and Hedging of Yield Curve Instruments

Jessica James, Michael Leister, Christoph Rieger

This is a test

This is a test

Partager le livre

196 pages

English

ePUB (adapté aux mobiles)

Disponible sur iOS et Android

eBook - ePub

Random Walks in Fixed Income and Foreign Exchange

Unexpected Discoveries in Issuance, Investment and Hedging of Yield Curve Instruments

Jessica James, Michael Leister, Christoph Rieger

Détails du livre

Aperçu du livre

Table des matières

Citations

À propos de ce livre

The fixed income and foreign exchange (FX) markets have never been as challenging to operate in as they are today. The post-crash combination of reduced liquidity, higher operating costs, low interest rates, flat yield curves and increased regulation means that market makers and investors alike need to work harder to generate value and remain in full understanding of the markets.

Random Walks in Fixed Income and Foreign Exchange brings together the best of detailed and original practitioner-orientated market research on many specialist areas of the bond and FX markets. Written by the highly regarded FX and bonds research desk at Commerzbank, the book offers varied and in-depth insight into specific topics of vital important to dealers and investors, including the cross-currency basis and hedging, the yield curve, and overseas issuance conversion factors which will give investors a genuine edge in generating value. Written in accessible text, it is a must-read for all those interested in bonds and FX.

Foire aux questions

Comment puis-je résilier mon abonnement ?

Il vous suffit de vous rendre dans la section compte dans paramètres et de cliquer sur « Résilier l’abonnement ». C’est aussi simple que cela ! Une fois que vous aurez résilié votre abonnement, il restera actif pour le reste de la période pour laquelle vous avez payé. Découvrez-en plus ici.

Puis-je / comment puis-je télécharger des livres ?

Pour le moment, tous nos livres en format ePub adaptés aux mobiles peuvent être téléchargés via l’application. La plupart de nos PDF sont également disponibles en téléchargement et les autres seront téléchargeables très prochainement. Découvrez-en plus ici.

Quelle est la différence entre les formules tarifaires ?

Les deux abonnements vous donnent un accès complet à la bibliothèque et à toutes les fonctionnalités de Perlego. Les seules différences sont les tarifs ainsi que la période d’abonnement : avec l’abonnement annuel, vous économiserez environ 30 % par rapport à 12 mois d’abonnement mensuel.

Qu’est-ce que Perlego ?

Nous sommes un service d’abonnement à des ouvrages universitaires en ligne, où vous pouvez accéder à toute une bibliothèque pour un prix inférieur à celui d’un seul livre par mois. Avec plus d’un million de livres sur plus de 1 000 sujets, nous avons ce qu’il vous faut ! Découvrez-en plus ici.

Prenez-vous en charge la synthèse vocale ?

Recherchez le symbole Écouter sur votre prochain livre pour voir si vous pouvez l’écouter. L’outil Écouter lit le texte à haute voix pour vous, en surlignant le passage qui est en cours de lecture. Vous pouvez le mettre sur pause, l’accélérer ou le ralentir. Découvrez-en plus ici.

Est-ce que Random Walks in Fixed Income and Foreign Exchange est un PDF/ePUB en ligne ?

Oui, vous pouvez accéder à Random Walks in Fixed Income and Foreign Exchange par Jessica James, Michael Leister, Christoph Rieger en format PDF et/ou ePUB ainsi qu’à d’autres livres populaires dans Volkswirtschaftslehre et Banken & Bankwesen. Nous disposons de plus d’un million d’ouvrages à découvrir dans notre catalogue.

Chapter 1 What Really is the Cross-Currency Basis?

The cross-currency basis – often just called the ‘basis’ – is a strange creature.1 It is referred to often enough in the financial markets that most participants think that they probably ought to know what it is. I was certainly one of them. ‘Some credit adjustment to currency hedging’ was how I vaguely thought of it. However, the more one studies and understands it, the stranger and more important it becomes. It is nothing less than a violation of the arbitrage conditions governing the relationships between interest rates and foreign exchange rates, and before it was observed, it would have been thought of as impossible. This paper describes how to calculate the basis, discusses some potential drivers, and ends with some unexpected applications.

The story of cross-currency basis swaps originates with the start of the floating currency market regime in the late 1970s and early 1980s, as corporations and investors with global reach sought methods of insuring themselves against sharp currency movements. Forward FX rate contracts became popular. The forward rate calculation is trivial (see equation (1)), and any deviation in the market from the calculated rate implied by interest rate differentials gives traders a chance to do arbitrage trades, which made such deviations unlikely.

And yet, since 2008, such deviations have persistently emerged. It is these deviations, expressed in a spread to one of the Libor interest rates used to calculate the forward FX rate, which are known as the cross-currency bases. We plot the basis for EURUSD in Figure 1.1; it is remarkable how large and persistent it can be, given that before 2008, arbitrage activity maintained it at almost zero.

Source: Commerzbank Research, Bloomberg

Figure 1.1: 1y EURUSD xccy basis.

The Calculation Underlying the Cross-Currency Basis Swap

A Quick Note on Terminology

An FX forward is a contract that locks in the price at which a counterparty can buy or sell a currency on a future date. The exchange rate is typically today’s rate, adjusted for the interest rate differential in the two currencies. If the interest rate in the local currency is higher than that of the USD (or whatever the reference currency is), the FX forward will include a devaluation expectation.

In a cross-currency swap, the parties exchange a stream of cashflows in one currency for a stream of cashflows in another. The typical cross-currency swap involves the exchange of both recurring interest and principal (usually at the end of the swap), and thus can fully cover the currency risk of a loan transaction. Conceptually, cross-currency swaps can be viewed as a series of forward contracts packaged together. For much more detail on more of these, see Appendix 1.B.

Perhaps the Simplest Formula in Financial Mathematics

The calculation to discover the forward rate is trivial. It is found using the following expression:

(1)

where F is the forward FX rate, S is the spot (current) FX rate, rf is the foreign interest rate and rd is the domestic interest rate. The FX rate must be quoted as units of foreign currency per domestic currency – for example, 1.1 USD (US dollar) per EUR (Euro). EURUSD is the conventional way of naming this rate in the market.

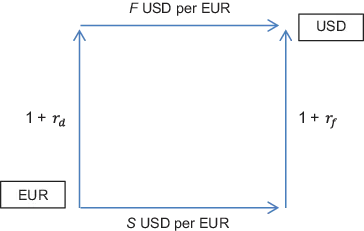

This calculation arises very simply. There are two ways of getting from holding the domestic currency now, to holding the foreign currency in the future, illustrated in Figure 1.2.

Method 1. Invest now for the period in question, at the domestic interest rate, then exchange at the end of the period.

Method 2. Exchange now so that you hold the foreign currency, and invest at the foreign currency rate for the period.

Figure 1.2: Forward FX rate calculation.

Arbitrage pricing would tell us that Method 1 and Method 2 must be exactly the same, apart from perhaps some small trading spread effects, or there will be a chance to ‘round trip’ the system and make some risk-free money (arbitrage). Conventionally, and in the pre-crisis world, this will only occur in a small and transient manner, as sharp-eyed traders look out for the chance and thus keep pressure on the forward rate to comply with equation (1).

This type of situation has traditionally (pre-crisis) arisen in small and temporary forms, quickly eliminated by arbitrage trading. Thus this method of calculating the forward rate was thought to be completely robust. How could it possibly be incorrect in any substantial way?

But as we will see, even this apparently unbreakable piece of mathematics is vulnerable to unforeseen market effects. The existence of a non-zero cross-currency basis ‘breaks’ equation (1).

How the Calculation Distorts No-Arbitrage Pricing

The relationship in equation (1) is protected by arbitrage constraints, which one would think, in this era where both humans and machines comb the market for strategies and opportunities, would be sufficient to ensure its integrity. However, market size and liquidity are not enough to ensure perfect efficiency. In Appendix 1.A, we show that the FX market has by some definitions been markedly inefficient since its origins as a floating rate, by allowing a profitable carry trade to persist. And we can present simple evidence that an acute distortion of equation (1) has occurred and moreover persists to this day.

Let us go back to the equation.

(1)

If EUR is the domestic currency, and USD the foreign currency, then a quick rearrangement gives us the following equation:

(2)

Now, all of these rates are readily observable in the market. To check it out precisely, we calculated rd using equation (2), and compared it to the market rate since 2000. Before about 2008, the calculated value of rd matches the value of rd obtained from the time series EUSW1V3 Curncy (on Bloomberg), the EUR 1-year swap rate. But after that dat...