Building Societies in the Financial Services Industry

Barbara Casu, Andrew Gall

This is a test

This is a test

Partager le livre

English

ePUB (adapté aux mobiles)

Disponible sur iOS et Android

eBook - ePub

Building Societies in the Financial Services Industry

Barbara Casu, Andrew Gall

Détails du livre

Aperçu du livre

Table des matières

Citations

À propos de ce livre

This book presents an analysis of the role of UK building societies, their strengths and weaknesses, and their contribution to the industry, at a time where public confidence in banking is low. Chapters present the results of an empirical analysis of the comparative performance of UK building societies, since the large-scale demutualisation process ended in the year 2000. The authors highlight the substantial impact of the financial crisis on the sector, with 2008 and 2009 being particularly difficult years. The book discusses banks and building societies in the context of the improving economy and show that both groups have recovered some profitability, although not at the pre-crisis level. The reader will discover that building societies in particular have recovered well from the financial turmoil and they appear less risky than banks on a variety of measures.

Foire aux questions

Comment puis-je résilier mon abonnement ?

Il vous suffit de vous rendre dans la section compte dans paramètres et de cliquer sur « Résilier l’abonnement ». C’est aussi simple que cela ! Une fois que vous aurez résilié votre abonnement, il restera actif pour le reste de la période pour laquelle vous avez payé. Découvrez-en plus ici.

Puis-je / comment puis-je télécharger des livres ?

Pour le moment, tous nos livres en format ePub adaptés aux mobiles peuvent être téléchargés via l’application. La plupart de nos PDF sont également disponibles en téléchargement et les autres seront téléchargeables très prochainement. Découvrez-en plus ici.

Quelle est la différence entre les formules tarifaires ?

Les deux abonnements vous donnent un accès complet à la bibliothèque et à toutes les fonctionnalités de Perlego. Les seules différences sont les tarifs ainsi que la période d’abonnement : avec l’abonnement annuel, vous économiserez environ 30 % par rapport à 12 mois d’abonnement mensuel.

Qu’est-ce que Perlego ?

Nous sommes un service d’abonnement à des ouvrages universitaires en ligne, où vous pouvez accéder à toute une bibliothèque pour un prix inférieur à celui d’un seul livre par mois. Avec plus d’un million de livres sur plus de 1 000 sujets, nous avons ce qu’il vous faut ! Découvrez-en plus ici.

Prenez-vous en charge la synthèse vocale ?

Recherchez le symbole Écouter sur votre prochain livre pour voir si vous pouvez l’écouter. L’outil Écouter lit le texte à haute voix pour vous, en surlignant le passage qui est en cours de lecture. Vous pouvez le mettre sur pause, l’accélérer ou le ralentir. Découvrez-en plus ici.

Est-ce que Building Societies in the Financial Services Industry est un PDF/ePUB en ligne ?

Oui, vous pouvez accéder à Building Societies in the Financial Services Industry par Barbara Casu, Andrew Gall en format PDF et/ou ePUB ainsi qu’à d’autres livres populaires dans Business et Servizi finanziari. Nous disposons de plus d’un million d’ouvrages à découvrir dans notre catalogue.

Barbara Casu and Andrew GallBuilding Societies in the Financial Services Industry10.1057/978-1-137-60208-4_1

Begin Abstract

1. Financial Services and the UK Economy

Barbara Casu1 and Andrew Gall2

(1)

Cass Business School-City University, London, UK

(2)

Building Societies Association, London, UK

Abstract

The UK financial services industry is undergoing a period of deep transformation, which affects all industry participants. This chapter reviews the impact of the global financial crisis on UK banking and discusses the events that lead to unprecedented government intervention and subsequent regulatory reforms. It also provides an overview of the changing structure of the UK banking and financial sectors. While UK banking is still dominated by few very large banking groups, the recent entrance of new banks has increased its competitive nature, particularly in the retail banking sector.

End Abstract

1.1 Introduction

The UK banking and financial sector has been severely impacted by the events of 2007–2008, which resulted in UK banks suffering big losses forcing significant government intervention in the sector. State aid was then followed by wide-ranging regulatory reforms, aimed at making the sector more resilient to shocks, by limiting risk-taking and improving bank conduct. The main outcome of the reform process has been the Financial Services (Banking Reform) Act of December 2013, which targets bank business models, with a view to “ring-fence” retail and wholesale banking activities.

The UK banking market is dominated by the presence of large banking groups: Lloyds, HSBC, the Royal Bank of Scotland (RBS), and Barclays control nearly 50 % of the mortgage market, 77 % of the personal current account market, and 85 % of small business banking (Molyneux 2016).

In the post-crisis banking landscape, political efforts to increase competition in the sector have led to new entry: in 2010, Metro Bank was the first to obtain a full banking licence in over a century and since then several new banks have been authorised by regulators (British Bankers’ Association 2014). These new entrants are referred to as challenger banks because they compete in a market dominated by long-established operators. Challenger banks have been remarkably successful in expanding their loan books and making some inroads in the retail market. This increased competition in the system, in addition to the effect of regulatory reforms, as well as far-reaching technological innovations, presents new challenges for the building societies sector.

Against this background, this chapter outlines the key events that impacted the UK banking market since the outbreak of the global financial crisis in 2007. Section 1.2 provides a brief outlook of the UK; Section 1.3 discusses the impact of the global financial crisis on UK banking and financial markets. Section 1.4 examines the recent regulatory developments and structural reforms. Section 1.5 presents a brief analysis of the industry structure and performance and Section 1.6 concludes the chapter.

1.2 A Brief Overview of the UK Economy

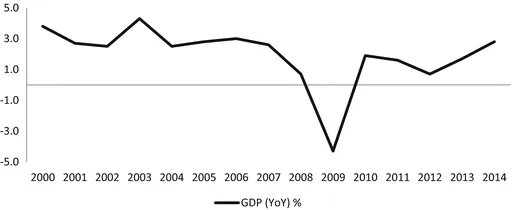

After more than a decade and a half of steady growth, the UK economy was officially declared to be in a recession in January 2009. The recession was a consequence of the credit crunch that began in the USA in August 2007 and which resulted in a global financial crisis starting in the autumn of 2008. It is now more than seven years since Lehman Brothers collapsed, ushering in the worst phase of the financial crisis, and the UK economy has been recovering at a relatively strong rate since early 2013 (Fig. 1.1).

Fig. 1.1

GDP growth (%) Year on Year (Source: Office for National Statistics (ONS) and authors’ calculations)

In 2014, the UK economy grew by 3.0 %, the fastest rate since 2007 and the strongest growth rate in the G7 group of countries (Office for National Statistics). UK growth has been driven primarily by services and is projected to continue at a solid pace in 2015 and 2016, boosted by domestic demand (Institute for Fiscal Studies (IFS)). There are still, however, causes for concern. For example, while the household debt-to-income (DTI) ratio has fallen over the last three years, it remains around 150 %, significantly higher than those of other European countries and the USA.

After several false starts following the financial crisis, the UK economy seems to be enjoying a period of sustained strong growth, helped by low oil prices, low inflation boosting purchasing power, and low interest rates fostering investment. It is expected that the low cost of finance will help maintain domestic demand growth. Rising house prices have also supported consumer confidence and spending (Fig. 1.2 and Table 1.1).

Fig. 1.2

UK average house prices (Source: Office for National Statistics (ONS) and authors’ calculations)

Table 1.1

Economic Indicators

Economic growth (YoY, %)

Inflation (YoY, %)

Household income

GDP

CPI

RPIX

RPI

Real household disposable income (YoY, %)

Saving ratio (%)

Household debt-to-income ratio (%)

2000

3.8

0.8

2.1

3

6.5

9.8

112

2001

2.7

1.2

2.1

1.8

4.9

10.7

119

2002

2.5

1.3

2.2

1.7

2.7

9.9

130

2003

4.3

1.4

2.8

2.9

2.7

9.2

141

2004

2.5

1.3

2.2

3

1.2

7.7

152

2005

2.8

2.1

2.3

2.8

2.1

7

154

2006

3

2.3

2.9

3.2

1.8

6.5

164

2007

2.6

2.3

3.2

4.3

2.4

7.1

168

2008

0.7

3.6

4.3

4

−0.6

5.6

167

2009

−4.3

2.2

2

−0.5

2.3

9.3

159

2010

1.9

3.3

4.8

4.6

0.9

11

151

2011

1.6

4.5

5.3

5.2

−1.9

8.6

150

2012

0.7

2.8

3.2

3.2

1.6

8

147

2013

1.7

2.6

3.1

3

−0.2

6.4

147

2014

3.0

1.5

2.4

2.4

1.5

6.0

144

Source: Office for National Statistics (ONS), Bank of England, and authors’ calculations. YoY = Year on Year

Although the UK economy is continuing to recover, the recession triggered by the global financial crisis had serious repercussion in many areas. UK banking was hit dramatically by the global financial crisis. A once profitable, innovative, and dynamic industry virtually collapsed, exposing a series of weaknesses that increased the severity of the crisis and its impact on the UK...