Option Pricing In Incomplete Markets: Modeling Based On Geometric L'evy Processes And Minimal Entropy Martingale Measures

Modeling Based on Geometric Lévy Processes and Minimal Entropy Martingale Measures

Yoshio Miyahara

This is a test

This is a test

Condividi libro

200 pagine

English

ePUB (disponibile sull'app)

Disponibile su iOS e Android

eBook - ePub

Option Pricing In Incomplete Markets: Modeling Based On Geometric L'evy Processes And Minimal Entropy Martingale Measures

Modeling Based on Geometric Lévy Processes and Minimal Entropy Martingale Measures

Yoshio Miyahara

Dettagli del libro

Anteprima del libro

Indice dei contenuti

Citazioni

Informazioni sul libro

This volume offers the reader practical methods to compute the option prices in the incomplete asset markets. The [GLP & MEMM] pricing models are clearly introduced, and the properties of these models are discussed in great detail. It is shown that the geometric Lévy process (GLP) is a typical example of the incomplete market, and that the MEMM (minimal entropy martingale measure) is an extremely powerful pricing measure.

This volume also presents the calibration procedure of the [GLP \& MEMM] model that has been widely used in the application of practical problems.

Contents:

Basic Concepts in Mathematical Finance

Lévy Processes and Geometric Lévy Process Models

Equivalent Martingale Measures

Esscher Transformed Martingale Measures

Minimax Martingale Measures and Minimal Distance Martingale Measures

Minimal Distance Martingale Measures for Geometric Lévy Processes

The [GLP & MEMM] Pricing Model

Calibration and Fitness Analysis of the [GLP & MEMM] Model

The [GSP & MEMM] Pricing Model

The Multi-Dimensional [GLP & MEMM] Pricing Model

Readership: Academics, graduate students and practitioners in mathematical finance.

Domande frequenti

Come faccio ad annullare l'abbonamento?

È semplicissimo: basta accedere alla sezione Account nelle Impostazioni e cliccare su "Annulla abbonamento". Dopo la cancellazione, l'abbonamento rimarrà attivo per il periodo rimanente già pagato. Per maggiori informazioni, clicca qui

È possibile scaricare libri? Se sì, come?

Al momento è possibile scaricare tramite l'app tutti i nostri libri ePub mobile-friendly. Anche la maggior parte dei nostri PDF è scaricabile e stiamo lavorando per rendere disponibile quanto prima il download di tutti gli altri file. Per maggiori informazioni, clicca qui

Che differenza c'è tra i piani?

Entrambi i piani ti danno accesso illimitato alla libreria e a tutte le funzionalità di Perlego. Le uniche differenze sono il prezzo e il periodo di abbonamento: con il piano annuale risparmierai circa il 30% rispetto a 12 rate con quello mensile.

Cos'è Perlego?

Perlego è un servizio di abbonamento a testi accademici, che ti permette di accedere a un'intera libreria online a un prezzo inferiore rispetto a quello che pagheresti per acquistare un singolo libro al mese. Con oltre 1 milione di testi suddivisi in più di 1.000 categorie, troverai sicuramente ciò che fa per te! Per maggiori informazioni, clicca qui.

Perlego supporta la sintesi vocale?

Cerca l'icona Sintesi vocale nel prossimo libro che leggerai per verificare se è possibile riprodurre l'audio. Questo strumento permette di leggere il testo a voce alta, evidenziandolo man mano che la lettura procede. Puoi aumentare o diminuire la velocità della sintesi vocale, oppure sospendere la riproduzione. Per maggiori informazioni, clicca qui.

Option Pricing In Incomplete Markets: Modeling Based On Geometric L'evy Processes And Minimal Entropy Martingale Measures è disponibile online in formato PDF/ePub?

Sì, puoi accedere a Option Pricing In Incomplete Markets: Modeling Based On Geometric L'evy Processes And Minimal Entropy Martingale Measures di Yoshio Miyahara in formato PDF e/o ePub, così come ad altri libri molto apprezzati nelle sezioni relative a Mathématiques e Mathématiques appliquées. Scopri oltre 1 milione di libri disponibili nel nostro catalogo.

In this chapter, we give an overview of basic concepts in mathematical finance theory, and then explain those concepts in very simple cases, namely in the single-term finite market.

1.1 Price Processes

Price processes of financial assets are usually modeled as stochastic processes. So mathematical finance theory is based on probability theory, particularly on the theory of stochastic processes.

The price process of an underlying asset is generally denoted by St in this book. The process St is usually assumed to be positive and is expressed in the following form

The time parameter t usually runs in [0, T], T > 0, or [0, ∞), and sometimes we consider the discrete time case (t = 0, 1, . . . , T).

1.2 No-arbitrage and Martingale Measures

In mathematical finance theory, properties of the market where the financial assets are traded are vitally important. If the market works well, then the economy should work well, but if the market does not work well, then the economy shouldn't work.

An important property of the market is its efficiency. This is the “no-arbitrage” or “no free lunch” assumption in mathematical finance theory. A brief definition of arbitrage is: “an arbitrage opportunity is the possibility to make a profit in a financial market without risk and without net investment of capital” (see Delbaen and Schachermayer [30] p.4). The no-arbitrage assumption means that a market does not allow any arbitrage opportunity. The theory which is constructed on the no-arbitrage assumption is called “arbitrage theory”. In arbitrage theory, the martingale measure plays an essential role.

1.3 Complete and Incomplete Markets

If the market has enough commodities, then a new commodity should be a replica of old ones, and we don't need other new commodities. This concept of sufficient commodities in the market is the meaning of completeness in the market.

1.4 Fundamental Theorems

The two concepts introduced above are characterized by the concept of the martingale measure. The following two theorems are well known. (See Delbaen and Schachermayer (2006) [30] or Bjçork (2004) [9] for details.)

Theorem 1.1. (First Fundamental Theorem in Mathematical Finance). A necessary and sufficient condition for the absence of arbitrage opportunities is the existence of the martingale measure of the underlying asset process.

Theorem 1.2. (Second Fundamental Theorem in Mathematical Finance). Assume the absence of arbitrage opportunities. Then a necessary and sufficient condition for the completeness of the market is the uniqueness of the martingale measure.

If the market is arbitrage-free and complete, then the price of a contingent claim B, ° (B), is determined by

where Q is the unique martingale measure and r is the interest rate of the bond. In the case where the market satisfies the no-arbitrage assumption but does not satisfy the completeness assumption, then the price °(B) is supposed to be in the following interval:

where M is the set of all equivalent martingale measures. (See Theorem 2.4.1 in Delbaen and Schachermayer [30].)

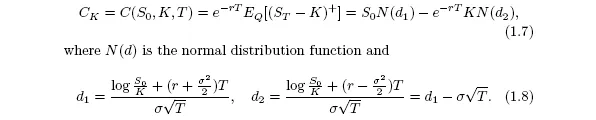

1.5 The Black Scholes Model

The most popular and fundamental model in mathematical finance is the Black-Scholes model (geometric Brownian motion model). The explicit form of the underlying asset process of this model is given by

or equivalently in the stochastic differential equation (SDE) form

where µ is a real number, σ is a positive real number, and Wt is a Wiener process (standard Brownian motion).

The risk-neutral measure (= martingale measure) Q is uniquely determined by Girsanov's theorem. Under Q the process

is a Wiener process and the price process St is expressed in the form

where r is the constant interest rate of a risk-free asset. The price of an option X is given by e−rT EQ [X]. The theoretical Black-Scholes price of the European call option, C (S0, K, T), with the strike price K and the fixed maturity T is given by the following formula: