Option Pricing In Incomplete Markets: Modeling Based On Geometric L'evy Processes And Minimal Entropy Martingale Measures

Modeling Based on Geometric Lévy Processes and Minimal Entropy Martingale Measures

Yoshio Miyahara

This is a test

This is a test

Buch teilen

200 Seiten

English

ePUB (handyfreundlich)

Über iOS und Android verfügbar

eBook - ePub

Option Pricing In Incomplete Markets: Modeling Based On Geometric L'evy Processes And Minimal Entropy Martingale Measures

Modeling Based on Geometric Lévy Processes and Minimal Entropy Martingale Measures

Yoshio Miyahara

Angaben zum Buch

Buchvorschau

Inhaltsverzeichnis

Quellenangaben

Über dieses Buch

This volume offers the reader practical methods to compute the option prices in the incomplete asset markets. The [GLP & MEMM] pricing models are clearly introduced, and the properties of these models are discussed in great detail. It is shown that the geometric Lévy process (GLP) is a typical example of the incomplete market, and that the MEMM (minimal entropy martingale measure) is an extremely powerful pricing measure.

This volume also presents the calibration procedure of the [GLP \& MEMM] model that has been widely used in the application of practical problems.

Contents:

Basic Concepts in Mathematical Finance

Lévy Processes and Geometric Lévy Process Models

Equivalent Martingale Measures

Esscher Transformed Martingale Measures

Minimax Martingale Measures and Minimal Distance Martingale Measures

Minimal Distance Martingale Measures for Geometric Lévy Processes

The [GLP & MEMM] Pricing Model

Calibration and Fitness Analysis of the [GLP & MEMM] Model

The [GSP & MEMM] Pricing Model

The Multi-Dimensional [GLP & MEMM] Pricing Model

Readership: Academics, graduate students and practitioners in mathematical finance.

Häufig gestellte Fragen

Wie kann ich mein Abo kündigen?

Gehe einfach zum Kontobereich in den Einstellungen und klicke auf „Abo kündigen“ – ganz einfach. Nachdem du gekündigt hast, bleibt deine Mitgliedschaft für den verbleibenden Abozeitraum, den du bereits bezahlt hast, aktiv. Mehr Informationen hier.

(Wie) Kann ich Bücher herunterladen?

Derzeit stehen all unsere auf Mobilgeräte reagierenden ePub-Bücher zum Download über die App zur Verfügung. Die meisten unserer PDFs stehen ebenfalls zum Download bereit; wir arbeiten daran, auch die übrigen PDFs zum Download anzubieten, bei denen dies aktuell noch nicht möglich ist. Weitere Informationen hier.

Welcher Unterschied besteht bei den Preisen zwischen den Aboplänen?

Mit beiden Aboplänen erhältst du vollen Zugang zur Bibliothek und allen Funktionen von Perlego. Die einzigen Unterschiede bestehen im Preis und dem Abozeitraum: Mit dem Jahresabo sparst du auf 12 Monate gerechnet im Vergleich zum Monatsabo rund 30 %.

Was ist Perlego?

Wir sind ein Online-Abodienst für Lehrbücher, bei dem du für weniger als den Preis eines einzelnen Buches pro Monat Zugang zu einer ganzen Online-Bibliothek erhältst. Mit über 1 Million Büchern zu über 1.000 verschiedenen Themen haben wir bestimmt alles, was du brauchst! Weitere Informationen hier.

Unterstützt Perlego Text-zu-Sprache?

Achte auf das Symbol zum Vorlesen in deinem nächsten Buch, um zu sehen, ob du es dir auch anhören kannst. Bei diesem Tool wird dir Text laut vorgelesen, wobei der Text beim Vorlesen auch grafisch hervorgehoben wird. Du kannst das Vorlesen jederzeit anhalten, beschleunigen und verlangsamen. Weitere Informationen hier.

Ist Option Pricing In Incomplete Markets: Modeling Based On Geometric L'evy Processes And Minimal Entropy Martingale Measures als Online-PDF/ePub verfügbar?

Ja, du hast Zugang zu Option Pricing In Incomplete Markets: Modeling Based On Geometric L'evy Processes And Minimal Entropy Martingale Measures von Yoshio Miyahara im PDF- und/oder ePub-Format sowie zu anderen beliebten Büchern aus Mathématiques & Mathématiques appliquées. Aus unserem Katalog stehen dir über 1 Million Bücher zur Verfügung.

In this chapter, we give an overview of basic concepts in mathematical finance theory, and then explain those concepts in very simple cases, namely in the single-term finite market.

1.1 Price Processes

Price processes of financial assets are usually modeled as stochastic processes. So mathematical finance theory is based on probability theory, particularly on the theory of stochastic processes.

The price process of an underlying asset is generally denoted by St in this book. The process St is usually assumed to be positive and is expressed in the following form

The time parameter t usually runs in [0, T], T > 0, or [0, ∞), and sometimes we consider the discrete time case (t = 0, 1, . . . , T).

1.2 No-arbitrage and Martingale Measures

In mathematical finance theory, properties of the market where the financial assets are traded are vitally important. If the market works well, then the economy should work well, but if the market does not work well, then the economy shouldn't work.

An important property of the market is its efficiency. This is the “no-arbitrage” or “no free lunch” assumption in mathematical finance theory. A brief definition of arbitrage is: “an arbitrage opportunity is the possibility to make a profit in a financial market without risk and without net investment of capital” (see Delbaen and Schachermayer [30] p.4). The no-arbitrage assumption means that a market does not allow any arbitrage opportunity. The theory which is constructed on the no-arbitrage assumption is called “arbitrage theory”. In arbitrage theory, the martingale measure plays an essential role.

1.3 Complete and Incomplete Markets

If the market has enough commodities, then a new commodity should be a replica of old ones, and we don't need other new commodities. This concept of sufficient commodities in the market is the meaning of completeness in the market.

1.4 Fundamental Theorems

The two concepts introduced above are characterized by the concept of the martingale measure. The following two theorems are well known. (See Delbaen and Schachermayer (2006) [30] or Bjçork (2004) [9] for details.)

Theorem 1.1. (First Fundamental Theorem in Mathematical Finance). A necessary and sufficient condition for the absence of arbitrage opportunities is the existence of the martingale measure of the underlying asset process.

Theorem 1.2. (Second Fundamental Theorem in Mathematical Finance). Assume the absence of arbitrage opportunities. Then a necessary and sufficient condition for the completeness of the market is the uniqueness of the martingale measure.

If the market is arbitrage-free and complete, then the price of a contingent claim B, ° (B), is determined by

where Q is the unique martingale measure and r is the interest rate of the bond. In the case where the market satisfies the no-arbitrage assumption but does not satisfy the completeness assumption, then the price °(B) is supposed to be in the following interval:

where M is the set of all equivalent martingale measures. (See Theorem 2.4.1 in Delbaen and Schachermayer [30].)

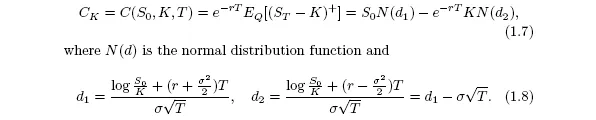

1.5 The Black Scholes Model

The most popular and fundamental model in mathematical finance is the Black-Scholes model (geometric Brownian motion model). The explicit form of the underlying asset process of this model is given by

or equivalently in the stochastic differential equation (SDE) form

where µ is a real number, σ is a positive real number, and Wt is a Wiener process (standard Brownian motion).

The risk-neutral measure (= martingale measure) Q is uniquely determined by Girsanov's theorem. Under Q the process

is a Wiener process and the price process St is expressed in the form

where r is the constant interest rate of a risk-free asset. The price of an option X is given by e−rT EQ [X]. The theoretical Black-Scholes price of the European call option, C (S0, K, T), with the strike price K and the fixed maturity T is given by the following formula: