IN THIS PART …

Check out what FinTech is, understand its impact, and look at the FinTech landscape.

Find out how FinTech has been disrupting the financial industry, challenging traditional financial institutions to “grow or die,” and creating opportunities for innovative start-up companies to claim a share of the pie.

Discover the role of regulation in FinTech, examine recent regulatory changes, and meet regulators in the United States and Europe.

IN THIS CHAPTER

Distinguishing FinTech’s dimensions Understanding financial technology changes Looking at the size of FinTech around the world Checking out important FinTech vocabulary FinTech has undoubtedly become one of the hottest topics in business. Web searches for the term fintech in Google have grown exponentially in the last several years, so it’s obvious that people are curious about it. But what is it, and why is it relevant to today’s financial industry? This chapter looks at those very basic questions, helping prepare you for the more detailed information you discover later in this book.

Having FinTech knowledge gives you a competitive advantage in your personal career, because FinTech experts are in high demand globally. Reading this book will also empower you to help your institution innovate and develop its services faster than your competitors. Globally, the FinTech market is booming, and we see investors investing across all stages of FinTech companies’ life cycles.

What Is FinTech, Anyway?

There are many definitions of FinTech, but for the purposes of this book, this one is the most relevant: FinTech companies are businesses that leverage new technology to create better financial services for both consumers and businesses. Of course, that begs another question: What is

financial technology? We define it as all

parts of technology that help provide financial services and products to customers. Those customers can be individuals, companies, or governments.

FinTech is also frequently used as an umbrella term for various subcategories, such as WealthTech and RegTech. You find out more about these subcategories in Chapter 2.

Analyzing FinTech’s Dimensions

FinTech may sound simple from the definition you read in the preceding section, but there are multiple dimensions. You need to think about each of these factors:

- Which part of finance is being impacted (financial sector)?

- Which business model is being used?

- Which technology is being used?

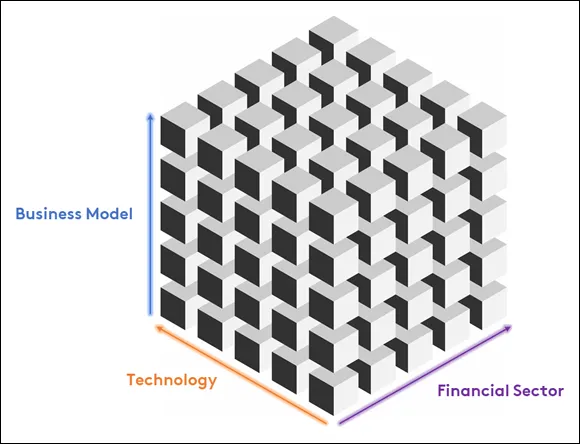

FINTECH Circle has coined the term Fintech Cube to describe the intersections of these factors. Figure 1-1 illustrates this cube, in which there are three axes: the financial sector on the x-axis, the business model on the y-axis, and technology on the z-axis.

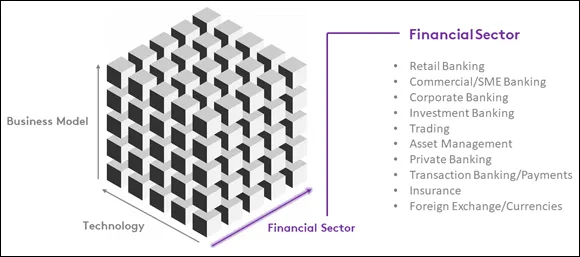

Each of these dimensions can be further categorized. For example, Figure 1-2 expands on the concept by adding key areas of financial services that can benefit from FinTech. All financial sectors are shown on one side of the cube, including retail banking, trading, and insurance (among others).

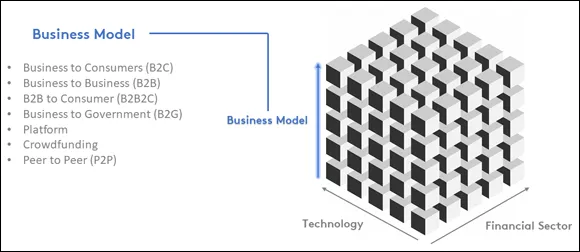

Figure 1-3 summarizes the most important business models from business-to-consumer (B2C), business-to-business (B2B), business-to-business-to-consumer (B2B2C), to business-to-government/regulator (B2G), to platform-based business models, crowdfunding, and peer-to-peer (P2P) lending.

Figure 1-4 shows the third dimension — the technology being used, which can range from cloud computing, big data, artificial intelligence (AI)/machine learning (ML), blockchain (distributed ledger technologies), the Internet of Things (IoT), and quantum computing, to augmented and virtual reality. Part 2 covers these technologies in more detail.

FinTech start-ups, for example, can now be more easily categorized and compared. For example, you may have a retail banking (financial sector x-axis) solution focused on the business model of B2C and using various technologies, such as cloud, big data analytics, and AI. Such a company would be called a challenger bank, sometimes also referred to as digital bank or neo-bank.