With the economy currently in turmoil, understanding how businesses and consumers interact is more important than ever—for business owners and students of economics, alike. A handy, fluff-free resource tool, our 3-panel (6-page) guide simplifies the world of microeconomics through the use of definitions, formulas and full-color tables and charts.

PRICE MAKER OR PRICE SEARCHER: The downward-sloping demand curve facing the monopolist is also the market demand curve.

Price must decline if the monopolist seeks to sell more. If the monopolist raises the price, the amount sold declines.

The monopolist can choose the price or the amount sold, but not both.

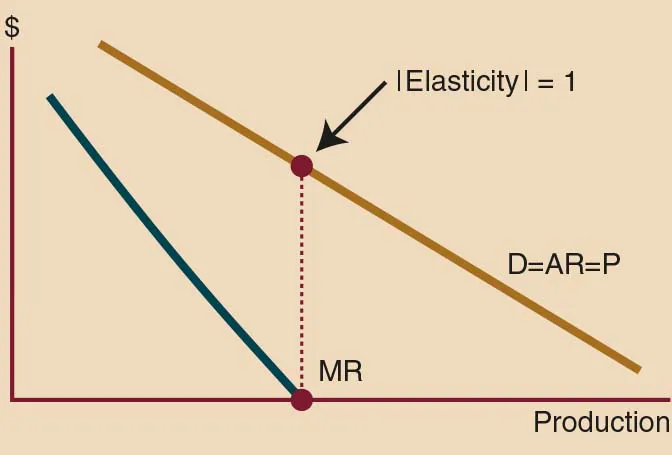

BECAUSE PRICE DECLINES AS OUTPUT ISEXPANDED, marginal revenue is less than price.

AT Q WHERE MR = 0,

Total revenue is maximized.

Elasticity of demand curve is unitary elastic.

BARRIERS TO ENTRY:

Strong legal barriers, patents and licenses.

Economies of scale keep out competition because the unit costs of a new entrant to the industry are much higher than the established monopolist who can charge lower prices.

Control of an essential resource can prevent competitors from entering the market.

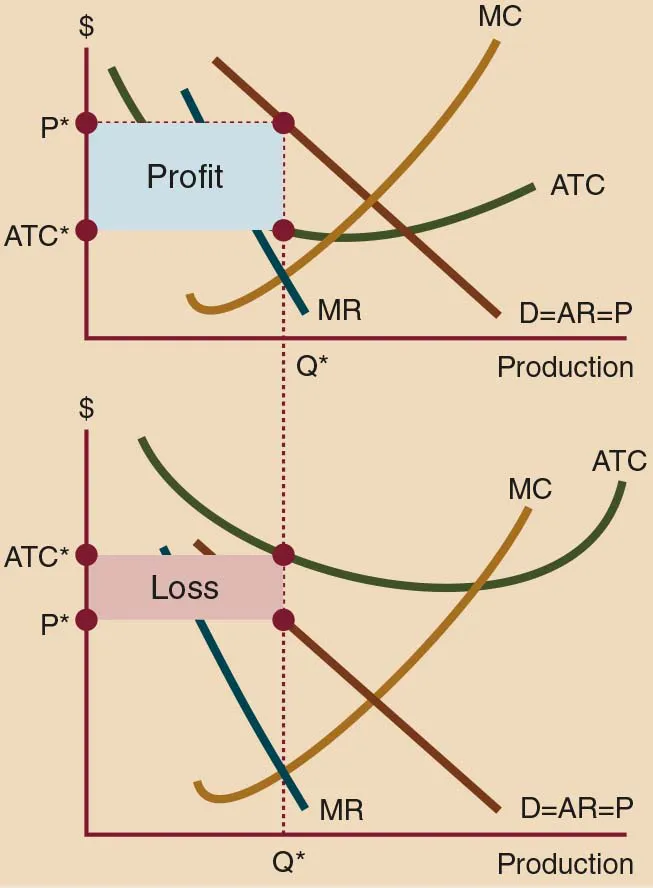

MONOPOLY PROFIT MAXIMIZATION

PRODUCTION: The monopolist expands production to Q*, until the revenue from the last marginal unit (marginal revenue) equals the cost of producing it (marginal cost).

PRICE: Once a level of production is selected, the demand curve gives the price (P*) that must be charged to persuade consumers to buy what is available.

PROFIT: Production will continue in the short run as long as the price exceeds the average variable cost.

If the price exceeds average variable cost (AVC) but is less than average total cost (ATC), the monopolist will produce at a loss.

If the price exceeds average total cost, the monopolist will make a profit.

In the long run, the monopolist can earn positive economic profits, but will shut down if it continues suffering losses.

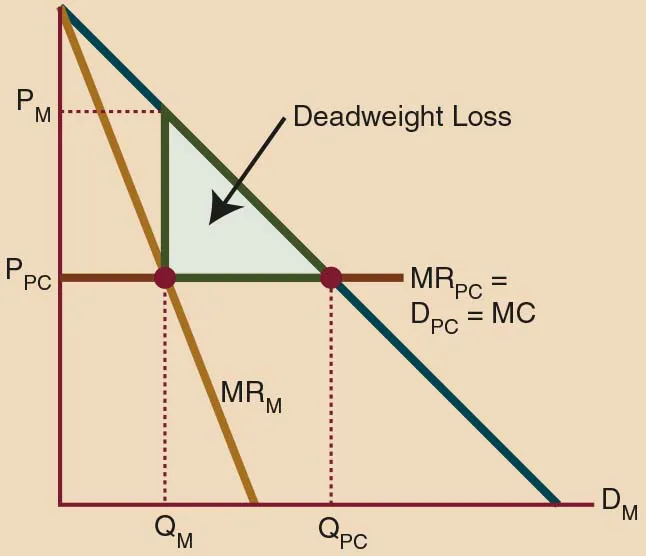

MONOPOLY & EFFICIENCY

THE MONOPOLIST IS NOT FORCED TOPRODUCE WHERE UNIT COSTS ARELOWEST (LACK OF COMPETITION). Thus, productive efficiency may not be achieved.

THE MONOPOLIST PRODUCES WHERETHE PRICE IS GREATER THAN THEMARGINAL COST. Hence, the consumer pays more for an extra unit of production thanit costs society. Allocative efficiency is not achieved.

MONOPOLISTS PRODUCE LESS ATA HIGHER PRICE THAN WOULDBE PRODUCED UNDER PERFECTCOMPETITION. Monopoly profit reduces consumer welfare by charging consumers a higher price. A reduction in production even further reduces their welfare; a “deadweight” loss to society is created.

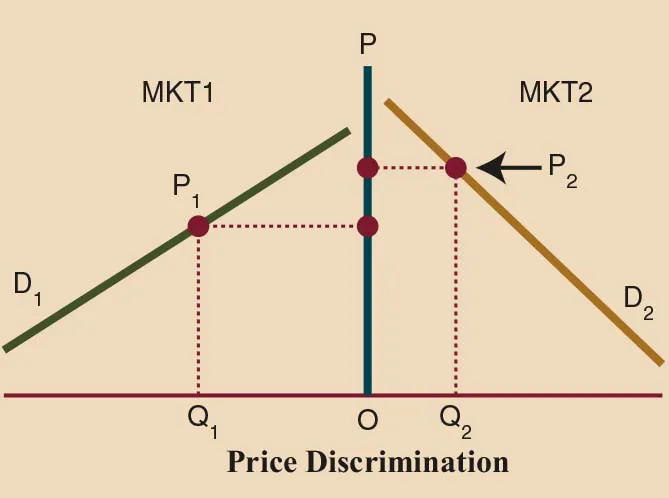

PRICE DISCRIMINATIONCHARGING CONSUMERS DIFFERENT PRICES FOR THE SAME PRODUCT.

REQUIREMENTS:

Seller must be a monopolist or have considerable monopoly power.

Sellers must be capable of dividing consumers into different classes, each class being charged a different price (market segmentation).

Marginal costs of production for the different classes must be similar.

Consumers charged a lower price must be incapable of reselling to consumers in the higher priced class.

FOR EACH CLASS OF CONSUMERS, THEMONOPOLIST SHOULD ALLOCATE OUTPUTTO THE POINT WHERE the marginal revenues from selling to each class are equal to the marginal costs.

Price discrimination reduces consumer surplus.

Perfect price discrimination completely wipes out consumer surplus.

NATURAL MONOPOLY

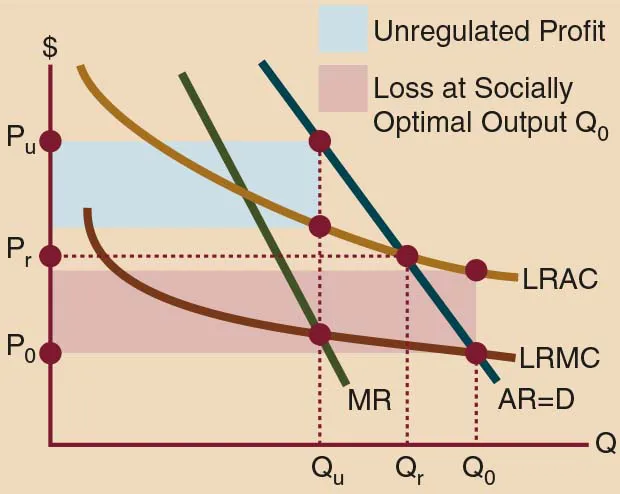

Definition: A natural monopoly arises because a single firm can supply the market and its long run average costs (LRAC) are still falling when the limits of market demand are reached. EX: Public Utilities.

UNREGULATED NATURAL MONOPOLY will produce QU(where MR = LRMC) at PU, making a profit.

There is no incentive for the monopolist to lower price and lower costs because of lack of competition.

The price will be raised to cover any cost increase.

There is uncertainty about where the true cost and demand curves lie.

SOCIALLY OPTIMAL OUTPUT (QO): D = LRMC. Here, allocative efficiency is achieved (output isproduced up to the point where the cost of an extra unitequals the price consumers are willing to pay for theextra unit). At QO, the price PO is less than LRAC and the monopolist realizes a loss. This requires a subsidy at least equal to the loss (which is most likely to occur if the government owns the firm).

PRIVATELY OWNED NATURAL MONOPOLIES ARE USUALLY REGULATED. The regulation allows the monopolist to charge Prand produce Qr, where the price equals LRAC. This ensures a “fair” return to the monopolist (normal profits).

PARTS OF A NATURAL MONOPOLY CAN BEOPENED TO COMPETITION. EX: A monopoly can be granted to the electric transmission system (wires, etc.) even if more than one company can produce the electricity to be generated.

MONOPOLISTIC COMPETITION

CHARACTERISTICS:

Large number of buyers and sellers

Imperfect information; price maker

Low barriers to entry

Differentiated products (such as different brands or levels of service); costs are higher due to expenditures to differentiate products (such as advertising)

Very elastic demand curve

Short run behavior like a monopo...

Table of contents

Overview

Supply & Demand

Shifts In The Supply & Demand Curves (Impact On Equilibrium)

Consumer Choice & Preference

Budget Line

Elasticity

Production Theory

Costs In The Short Run

Costs In The Long Run

Perfect Competition

Monopoly

Resource Markets

Wage Determination

Externalities

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Microeconomics by in PDF and/or ePUB format, as well as other popular books in Volkswirtschaftslehre & Business allgemein. We have over 1.5 million books available in our catalogue for you to explore.