This is a succinct guide to the application and modelling of dependence models or copulas in the financial markets. First applied to credit risk modelling, copulas are now widely used across a range of derivatives transactions, asset pricing techniques and risk models and are a core part of the financial engineer's toolkit.

Häufig gestellte Fragen

Wie kann ich mein Abo kündigen?

Gehe einfach zum Kontobereich in den Einstellungen und klicke auf „Abo kündigen“ – ganz einfach. Nachdem du gekündigt hast, bleibt deine Mitgliedschaft für den verbleibenden Abozeitraum, den du bereits bezahlt hast, aktiv. Mehr Informationen hier.

(Wie) Kann ich Bücher herunterladen?

Derzeit stehen all unsere auf Mobilgeräte reagierenden ePub-Bücher zum Download über die App zur Verfügung. Die meisten unserer PDFs stehen ebenfalls zum Download bereit; wir arbeiten daran, auch die übrigen PDFs zum Download anzubieten, bei denen dies aktuell noch nicht möglich ist. Weitere Informationen hier.

Welcher Unterschied besteht bei den Preisen zwischen den Aboplänen?

Mit beiden Aboplänen erhältst du vollen Zugang zur Bibliothek und allen Funktionen von Perlego. Die einzigen Unterschiede bestehen im Preis und dem Abozeitraum: Mit dem Jahresabo sparst du auf 12 Monate gerechnet im Vergleich zum Monatsabo rund 30 %.

Was ist Perlego?

Wir sind ein Online-Abodienst für Lehrbücher, bei dem du für weniger als den Preis eines einzelnen Buches pro Monat Zugang zu einer ganzen Online-Bibliothek erhältst. Mit über 1 Million Büchern zu über 1.000 verschiedenen Themen haben wir bestimmt alles, was du brauchst! Weitere Informationen hier.

Unterstützt Perlego Text-zu-Sprache?

Achte auf das Symbol zum Vorlesen in deinem nächsten Buch, um zu sehen, ob du es dir auch anhören kannst. Bei diesem Tool wird dir Text laut vorgelesen, wobei der Text beim Vorlesen auch grafisch hervorgehoben wird. Du kannst das Vorlesen jederzeit anhalten, beschleunigen und verlangsamen. Weitere Informationen hier.

Ist Financial Engineering with Copulas Explained als Online-PDF/ePub verfügbar?

Ja, du hast Zugang zu Financial Engineering with Copulas Explained von J. Mai, M. Scherer im PDF- und/oder ePub-Format sowie zu anderen beliebten Büchern aus Betriebswirtschaft & Finanzengineering. Aus unserem Katalog stehen dir über 1 Million Bücher zur Verfügung.

This chapter introduces a concept for describing the dependence structure between random variables with arbitrary marginal distribution functions. The main idea is to describe the probability distribution of a d-dimensional random vector by two separate objects: (i) the set of univariate probability distributions for all d components, the so-called ‘marginals’, and (ii) a ‘copula’, which is a d-variate function that contains the information about the dependence structure between the components. Although such a separation into marginals and a copula (if done carelessly) bears some potential for irritations (see Section 7.2 and [Mikosch (2006)]), it can be quite convenient in many applications. The rest of this chapter is organized as follows. Section 1.1 presents two examples which motivate the necessity for the use of a copula concept. Section 1.2 presents Sklar’s Theorem, which can be seen as the ‘fundamental theorem of copula theory’.

1.1 Two Motivating Examples

The following examples illustrate situations where it is convenient to separate univariate marginal distributions and dependence structure, which is precisely what the concept of a copula does.

1.1.1 Example 1: Analyzing Dependence between Asset Movements

We consider three time series with daily observations, ranging from April 2008 to May 2013: the stock price of BMW AG, the stock price of Daimler AG, and a Gold Index. Intuitively, we would expect the movements of Daimler and BMW to be highly dependent, whereas the returns of BMW and the Gold Index are expected to be much more weakly associated, if not independent. But how can we measure or visualize this dependence? To tackle this question, we introduce a little bit of probability theory by viewing the observed time series as realizations of certain stochastic processes. For the sake of notational convenience, we abbreviate to B = BMW, D = Daimler, and G = Gold. First, each individual time series

, for * ∈ {B, D, G}, is transformed to a return time series

via

, i = 0, 1, 2, . . . , n – 1. Next, we assume that the returns are realizations of independent and identically distributed (iid) random variables.1 More precisely, the vectors

, i = 1, . . . , n, are iid realizations of the random vector (R(B) , R(D) , R(G)). We want to analyze the dependence structure between the components of this random vector. Under these assumptions, the dependence between the movements of the BMW stock, the Daimler stock, and the Gold Index are completely described by the dependence between the random variables R(B), R(D), and R(G). For the mathematical description of this dependence there exists a rigorous theory, part of which is introduced in this book. We now provide a couple of intuitive ideas of what to do with our data.

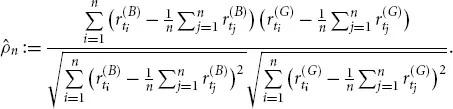

(a)Linear correlation: The notion of a ‘correlation coefficient’ is the kind of dependence measurement that is omnipresent in the literature as well as in daily practice. Given the two time series of BMW and Gold Index returns, their empirical (or historical) correlation coefficient is computed via the formula

Intuitively speaking, this is the empirical covariance divided by the empirical standard deviations. This number is known to lie between – 1 and +1, which are interpreted as the boundary values of a scale measuring the strength of dependence. The value – 1 is understood as negative dependence, the middle value 0 as uncorrelated, and the value +1 as positive dependence. Statistically speaking, the number

, which is computed only from observed data, is an estimate for the theoretical quantity

Generally speaking, the correlation coefficient ρ is one dependence measure (among many), and it is by far the most popular one. However, it has its shortcomings (see Chapter 3). Copula theory can help to overcome these limitations, because it provides a solid ground to axiomatically define dependence measures.

(b)Scatter plot: One of the most obvious approaches to visualize the dependence between the return variables, say R(B) and R(G), is to plot the observed historical data into a two-dimensional coordinate system, which is done in Figure 1.1. Such an illustration is called a ‘scatter plot’. In the same figure the scatter plots for the observed values of R(B) vs. R(D) and R(D) vs. R(G) are also provided in order to judge on the qualitative differences between the dependence structures. All scatter plots appear to be centered roughly around (0, 0); only the two automobile firms exhibit a scatter plot which is m...