This is a succinct guide to the application and modelling of dependence models or copulas in the financial markets. First applied to credit risk modelling, copulas are now widely used across a range of derivatives transactions, asset pricing techniques and risk models and are a core part of the financial engineer's toolkit.

Foire aux questions

Comment puis-je résilier mon abonnement ?

Il vous suffit de vous rendre dans la section compte dans paramètres et de cliquer sur « Résilier l’abonnement ». C’est aussi simple que cela ! Une fois que vous aurez résilié votre abonnement, il restera actif pour le reste de la période pour laquelle vous avez payé. Découvrez-en plus ici.

Puis-je / comment puis-je télécharger des livres ?

Pour le moment, tous nos livres en format ePub adaptés aux mobiles peuvent être téléchargés via l’application. La plupart de nos PDF sont également disponibles en téléchargement et les autres seront téléchargeables très prochainement. Découvrez-en plus ici.

Quelle est la différence entre les formules tarifaires ?

Les deux abonnements vous donnent un accès complet à la bibliothèque et à toutes les fonctionnalités de Perlego. Les seules différences sont les tarifs ainsi que la période d’abonnement : avec l’abonnement annuel, vous économiserez environ 30 % par rapport à 12 mois d’abonnement mensuel.

Qu’est-ce que Perlego ?

Nous sommes un service d’abonnement à des ouvrages universitaires en ligne, où vous pouvez accéder à toute une bibliothèque pour un prix inférieur à celui d’un seul livre par mois. Avec plus d’un million de livres sur plus de 1 000 sujets, nous avons ce qu’il vous faut ! Découvrez-en plus ici.

Prenez-vous en charge la synthèse vocale ?

Recherchez le symbole Écouter sur votre prochain livre pour voir si vous pouvez l’écouter. L’outil Écouter lit le texte à haute voix pour vous, en surlignant le passage qui est en cours de lecture. Vous pouvez le mettre sur pause, l’accélérer ou le ralentir. Découvrez-en plus ici.

Est-ce que Financial Engineering with Copulas Explained est un PDF/ePUB en ligne ?

Oui, vous pouvez accéder à Financial Engineering with Copulas Explained par J. Mai, M. Scherer en format PDF et/ou ePUB ainsi qu’à d’autres livres populaires dans Betriebswirtschaft et Finanzengineering. Nous disposons de plus d’un million d’ouvrages à découvrir dans notre catalogue.

This chapter introduces a concept for describing the dependence structure between random variables with arbitrary marginal distribution functions. The main idea is to describe the probability distribution of a d-dimensional random vector by two separate objects: (i) the set of univariate probability distributions for all d components, the so-called ‘marginals’, and (ii) a ‘copula’, which is a d-variate function that contains the information about the dependence structure between the components. Although such a separation into marginals and a copula (if done carelessly) bears some potential for irritations (see Section 7.2 and [Mikosch (2006)]), it can be quite convenient in many applications. The rest of this chapter is organized as follows. Section 1.1 presents two examples which motivate the necessity for the use of a copula concept. Section 1.2 presents Sklar’s Theorem, which can be seen as the ‘fundamental theorem of copula theory’.

1.1 Two Motivating Examples

The following examples illustrate situations where it is convenient to separate univariate marginal distributions and dependence structure, which is precisely what the concept of a copula does.

1.1.1 Example 1: Analyzing Dependence between Asset Movements

We consider three time series with daily observations, ranging from April 2008 to May 2013: the stock price of BMW AG, the stock price of Daimler AG, and a Gold Index. Intuitively, we would expect the movements of Daimler and BMW to be highly dependent, whereas the returns of BMW and the Gold Index are expected to be much more weakly associated, if not independent. But how can we measure or visualize this dependence? To tackle this question, we introduce a little bit of probability theory by viewing the observed time series as realizations of certain stochastic processes. For the sake of notational convenience, we abbreviate to B = BMW, D = Daimler, and G = Gold. First, each individual time series

, for * ∈ {B, D, G}, is transformed to a return time series

via

, i = 0, 1, 2, . . . , n – 1. Next, we assume that the returns are realizations of independent and identically distributed (iid) random variables.1 More precisely, the vectors

, i = 1, . . . , n, are iid realizations of the random vector (R(B) , R(D) , R(G)). We want to analyze the dependence structure between the components of this random vector. Under these assumptions, the dependence between the movements of the BMW stock, the Daimler stock, and the Gold Index are completely described by the dependence between the random variables R(B), R(D), and R(G). For the mathematical description of this dependence there exists a rigorous theory, part of which is introduced in this book. We now provide a couple of intuitive ideas of what to do with our data.

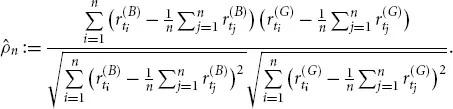

(a)Linear correlation: The notion of a ‘correlation coefficient’ is the kind of dependence measurement that is omnipresent in the literature as well as in daily practice. Given the two time series of BMW and Gold Index returns, their empirical (or historical) correlation coefficient is computed via the formula

Intuitively speaking, this is the empirical covariance divided by the empirical standard deviations. This number is known to lie between – 1 and +1, which are interpreted as the boundary values of a scale measuring the strength of dependence. The value – 1 is understood as negative dependence, the middle value 0 as uncorrelated, and the value +1 as positive dependence. Statistically speaking, the number

, which is computed only from observed data, is an estimate for the theoretical quantity

Generally speaking, the correlation coefficient ρ is one dependence measure (among many), and it is by far the most popular one. However, it has its shortcomings (see Chapter 3). Copula theory can help to overcome these limitations, because it provides a solid ground to axiomatically define dependence measures.

(b)Scatter plot: One of the most obvious approaches to visualize the dependence between the return variables, say R(B) and R(G), is to plot the observed historical data into a two-dimensional coordinate system, which is done in Figure 1.1. Such an illustration is called a ‘scatter plot’. In the same figure the scatter plots for the observed values of R(B) vs. R(D) and R(D) vs. R(G) are also provided in order to judge on the qualitative differences between the dependence structures. All scatter plots appear to be centered roughly around (0, 0); only the two automobile firms exhibit a scatter plot which is m...