eBook - ePub

An Option Greeks Primer

Building Intuition with Delta Hedging and Monte Carlo Simulation using Excel

Jawwad Farid

This is a test

Compartir libro

- English

- ePUB (apto para móviles)

- Disponible en iOS y Android

eBook - ePub

An Option Greeks Primer

Building Intuition with Delta Hedging and Monte Carlo Simulation using Excel

Jawwad Farid

Detalles del libro

Vista previa del libro

Índice

Citas

Información del libro

This book provides a hands-on, practical guide to understanding derivatives pricing. Aimed at the less quantitative practitioner, it provides a balanced account of options, Greeks and hedging techniques avoiding the complicated mathematics inherent to many texts, and with a focus on modelling, market practice and intuition.

Preguntas frecuentes

¿Cómo cancelo mi suscripción?

¿Cómo descargo los libros?

Por el momento, todos nuestros libros ePub adaptables a dispositivos móviles se pueden descargar a través de la aplicación. La mayor parte de nuestros PDF también se puede descargar y ya estamos trabajando para que el resto también sea descargable. Obtén más información aquí.

¿En qué se diferencian los planes de precios?

Ambos planes te permiten acceder por completo a la biblioteca y a todas las funciones de Perlego. Las únicas diferencias son el precio y el período de suscripción: con el plan anual ahorrarás en torno a un 30 % en comparación con 12 meses de un plan mensual.

¿Qué es Perlego?

Somos un servicio de suscripción de libros de texto en línea que te permite acceder a toda una biblioteca en línea por menos de lo que cuesta un libro al mes. Con más de un millón de libros sobre más de 1000 categorías, ¡tenemos todo lo que necesitas! Obtén más información aquí.

¿Perlego ofrece la función de texto a voz?

Busca el símbolo de lectura en voz alta en tu próximo libro para ver si puedes escucharlo. La herramienta de lectura en voz alta lee el texto en voz alta por ti, resaltando el texto a medida que se lee. Puedes pausarla, acelerarla y ralentizarla. Obtén más información aquí.

¿Es An Option Greeks Primer un PDF/ePUB en línea?

Sí, puedes acceder a An Option Greeks Primer de Jawwad Farid en formato PDF o ePUB, así como a otros libros populares de Business y Gestione di rischi finanziari. Tenemos más de un millón de libros disponibles en nuestro catálogo para que explores.

Información

Categoría

BusinessCategoría

Gestione di rischi finanziariPart I

Refresher

Introduction: Context

1 Options

A vanilla option is a derivative instrument that gives us the right to buy or sell an underlying security on a future date at a price agreed upon today. Unlike a forward or future contract, an option gives us the right to walk away if the market price is not in our favour. If we do decide to walk away, our loss is limited to the upfront premium we paid when we purchased the option.

The right to buy an underlying security is known as a call. The right to sell an underlying security is known as a put. When we sell an option we write it, and our obligation is very different from that of the buyer; while the buyer has the right to walk away, the writer is obligated to perform.

For a more detailed treatment of the Options and derivatives world, see John C. Hull, Paul Wilmott and Jawwad Farid.1

2 Option price drivers

Option prices are determined by a range of methods. Three of the methods that we will refer to in this book are the Black–Scholes equation (also known as the Black–Scholes–Merton Model or BSM for short) for European options; Binomial Trees for American options; and the Monte Carlo simulation.

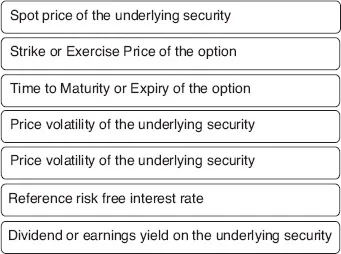

Irrespective of the method used, the price of an option is determined by the following factors:2

A natural follow-up question is: How does the price of an option change when any of the above variables changes? And then: Which of these variables has the biggest price impact, and which the least?

3 Greeks

Greeks are approximations used to determine the change in price of the option due to a unit change in the value of one of the above drivers. They are also known as option price sensitivities (OPS) or option factor sensitivities. They are called Greeks because their names reference the Greek alphabet: Delta, Gamma, Vega, Theta and Rho.

If you are familiar with the world of fixed income investment you will have heard of the terms ‘duration’ and ‘convexity’, which measure the change in the value of a treasury bond for a change in the underlying interest rates. Duration is a first-order (linear) rate of change in the price of an interest-rate-sensitive instrument (a bond) because of a change in the yield to maturity or reference rate of the instrument. Convexity is a second-order (non-linear) derivative that adjusts the linear sensitivity measure to account for the curvature in the price–yield relationship. In like manner, there are multiple option price sensitivities because of multiple option price drivers. Some, like duration for fixed income securities, are linear (e.g. Delta). Others, like convexity for fixed income securities, are non-linear (e.g. Gamma).

4 Hedging and squaring

Trading desks make money by taking (running) positions for their account, buying and selling at a spread (buying low, selling high) or market making (providing liquidity by holding an instrument on their balance sheet temporarily). In order for them to buy and sell at a spread they need to offset (hedge) their client positions. This process of matching or offsetting positions is called squaring. The spread is booked and realized when they buy (long) from the client at a slightly lower price and then sell (short) in the market at a slightly higher price, and vice versa.

If no appropriate counterparty or security is available to hedge a position, a trader needs to hedge their exposure by using basic principles. An unhedged position is known as an open (or naked) position.

5 Empirical and implied volatility

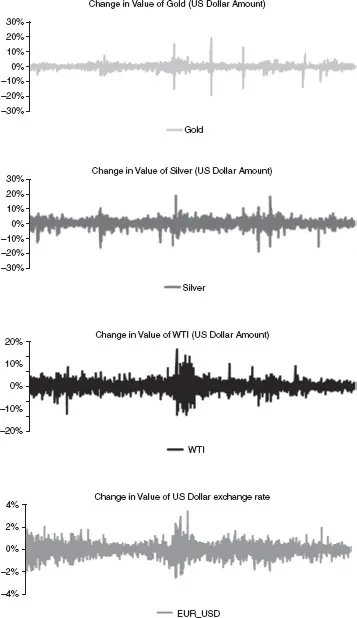

Within the options world, volatility is a measure of relative price changes. These changes can be measured on a daily, weekly, monthly or annualized basis. When volatility is measured using actual historical price data, we call it empirical or historical volatility. Figure 1 illustrates the behaviour of historical volatility for Gold, Silver, WTI and the EUR-USD exchange rate.

The volatility used as an input to determine option prices is not historical or empirical volatility, but implied volatility. While historical volatility is the historical average, implied volatility represents a mixture of future expectations of realized volatility and the level of volatility at which a trader is comfortable taking a position.

Figure 1 Changes in gold, silver, WTI and US dollar prices

Source: The Greeks against Spot. FinanceTrainingCourse.com

...