eBook - ePub

Modern Derivatives Pricing and Credit Exposure Analysis

Theory and Practice of CSA and XVA Pricing, Exposure Simulation and Backtesting

Roland Lichters, Roland Stamm, Donal Gallagher

This is a test

Compartir libro

- English

- ePUB (apto para móviles)

- Disponible en iOS y Android

eBook - ePub

Modern Derivatives Pricing and Credit Exposure Analysis

Theory and Practice of CSA and XVA Pricing, Exposure Simulation and Backtesting

Roland Lichters, Roland Stamm, Donal Gallagher

Detalles del libro

Vista previa del libro

Índice

Citas

Información del libro

This book provides a comprehensive guide for modern derivatives pricing and credit analysis. Written to provide sound theoretical detail but practical implication, it provides readers with everything they need to know to price modern financial derivatives and analyze the credit exposure of a financial instrument in today's markets.

Preguntas frecuentes

¿Cómo cancelo mi suscripción?

¿Cómo descargo los libros?

Por el momento, todos nuestros libros ePub adaptables a dispositivos móviles se pueden descargar a través de la aplicación. La mayor parte de nuestros PDF también se puede descargar y ya estamos trabajando para que el resto también sea descargable. Obtén más información aquí.

¿En qué se diferencian los planes de precios?

Ambos planes te permiten acceder por completo a la biblioteca y a todas las funciones de Perlego. Las únicas diferencias son el precio y el período de suscripción: con el plan anual ahorrarás en torno a un 30 % en comparación con 12 meses de un plan mensual.

¿Qué es Perlego?

Somos un servicio de suscripción de libros de texto en línea que te permite acceder a toda una biblioteca en línea por menos de lo que cuesta un libro al mes. Con más de un millón de libros sobre más de 1000 categorías, ¡tenemos todo lo que necesitas! Obtén más información aquí.

¿Perlego ofrece la función de texto a voz?

Busca el símbolo de lectura en voz alta en tu próximo libro para ver si puedes escucharlo. La herramienta de lectura en voz alta lee el texto en voz alta por ti, resaltando el texto a medida que se lee. Puedes pausarla, acelerarla y ralentizarla. Obtén más información aquí.

¿Es Modern Derivatives Pricing and Credit Exposure Analysis un PDF/ePUB en línea?

Sí, puedes acceder a Modern Derivatives Pricing and Credit Exposure Analysis de Roland Lichters, Roland Stamm, Donal Gallagher en formato PDF o ePUB, así como a otros libros populares de Volkswirtschaftslehre y Ökonometrie. Tenemos más de un millón de libros disponibles en nuestro catálogo para que explores.

Información

Categoría

VolkswirtschaftslehreCategoría

ÖkonometrieI

Discounting

1 | | Discounting Before the Crisis |

1.1 The risk-free rate

The main ingredient for pricing is the zero curve r(t) which assigns an interest rate to any given maturity t > 0. It tells us what the value of 1 currency unit will be at time t if invested at the risk-free rate. For most theoretical applications, the zero rate is expressed as continuously compounding, so the value at time t will be given by

Other conventions are also common. Linear compounding is typically used for short-term interest (less than one year):

Simple compounding takes interest on interest into account, in particular for maturities beyond one year:

Conversely, today’s value of one currency unit paid in t years is given by

P(0,t) is the price of a risk-free zero bond with maturity t, as seen today (at time 0). It is also referred to as the (deterministic) discount factor for time t, dft.

This immediately raises the question: What is the risk-free rate, which is the compensation to lenders for not using their money for consumption immediately? The person or institution making the promise of paying back the money would have to be seen as non-defaultable, no matter what happens. Obviously, such an entity does not exist, so people use proxies like certain highly rated governments or supra-national institutions. Before the near-default of Bear Stearns, people viewed banks that were rated AA or higher as virtually default-free, and therefore used the LIBOR rate as proxies for the risk-free rate.

1.2 Pricing linear instruments

1.2.1 Forward rate agreements

The most important building block in interest rate modelling is the forward rate agreement, or FRA for short. This is a contract by which two parties agree today (at t = 0) on an interest rate f(0;t1,t2) to be paid in t2 for a loan spanning a future period t1 to t2. If the market (i.e. LIBOR) rate L(t1,t2) which is fixed in t1 for that period exceeds f(0;t1,t2), the payer of the rate has made a profit. Otherwise, the receiver gains more than the market rate.

Market practice is that the payment is actually paid in t1 by computing the cash flow in t2 and discounting it to t1 with the fixed LIBOR rate. For pricing purposes, this is virtually irrelevant (see [117]), so we ignore this distinction.

Pricing this correctly is obviously equivalent to predicting the LIBOR rate in a market-accepted manner.

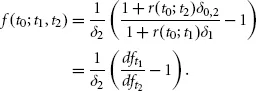

What rate can we expect in three months’ time if we want to borrow money for six months at that time? Calculate the forward rate of a 3M into 9M FRA as follows:

• Borrow df0.25 = P(0,0.25) units for three months at the risk-free three-month rate

• Invest the money for nine months at the risk-free rate for nine months

• Borrow 1 unit in an FRA in three months (maturing six months later) to pay back the loan with interest

• After another six months, pay back the loan with the df0.25/df0.75 from the investment

• By the no-arbitrage principle, the combination has to be worth 0. The forward rate therefore has to be

Note that, in general, the period lengths are not exactly a quarter or half a year but rather depend on the day count fraction of the rates used. In Euroland, this would be ACT/360, for example.

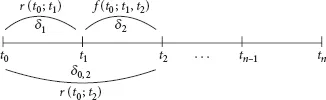

In Figure 1.1, we must have (assuming linear compounding, as is the market custom for periods of less than one year)

Figure 1.1 Replication of the forward rate

In other words

In general, the forward rate for time t (in years from today) for a period of δ (in years) is given by

The present value of the forward rate paid on a notional of 1 unit is therefore

Note that this is true because we use the same discount factors in the forward rate replication as when discounting cash flows. The main assumption in this replication argument is that I (at least a bank) can borrow and lend arbitrary amounts at the risk-free (LIBOR) rate.

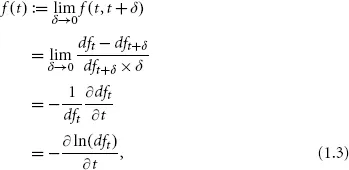

We can take a look at what happens if we let δ approach 0 in formula (1.1), under the assumption that the discount curve is differentiable:

which also implies that

Forward rates are used as expected values for the LIBOR fixing for a future time period. Most importantly, this is done in interest rate swaps.

1.2.2 Interest rate swaps

An interest rate swap, or swap for short, is a contract by which two parties agree to exchange interest payments on a predetermined notional on a regular basis. One party pays the fixed rate with the frequency which is standard in the chosen currency. For EUR, for instance, this is annually; for USD, on the other hand, this is semi-annually. The other party pays a floating rate linked to LIBOR of some given frequency (1, 3, 6 or 12 months), possibly with a spread. There is also a standard frequency for floating legs in most currencies: in EUR, this is six months, and in USD, it is three months, for instance.

At inception, the v...